TL;DR:

- Appraisals provide an independent estimate of a property's market value crucial for financing and transactions.

- Proper preparation and documentation can positively influence appraisal outcomes in Los Angeles and Orange County.

- Regional market factors and neighborhood specifics significantly impact appraisal results and potential deal success.

An appraisal can quietly determine whether your deal closes or falls apart. In Los Angeles and Orange County, where prices shift fast and competition is fierce, many buyers and investors walk into transactions without fully understanding how appraisals work or what they can do to influence the outcome. A number that comes in too low can stall financing, force renegotiations, or kill a deal entirely. This guide breaks down every essential part of the real estate appraisal process, from how it works and what appraisers actually look for, to how you can prepare your property and protect your investment in Southern California's high-stakes market.

Table of Contents

- What is a real estate appraisal and why does it matter?

- The appraisal process: Steps, factors, and who's involved

- Common challenges and how appraisals can kill or save a deal

- How to prepare for an appraisal: Maximizing your property's value

- Appraisals in Los Angeles and Orange County: Special considerations

- A local expert's perspective: What really makes appraisals succeed

- Get expert appraisal support with INC Realtors

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Appraisals protect investments | A third-party appraisal ensures that buyers and lenders pay a fair price based on current market value. |

| Multiple factors impact value | Comparable sales, property condition, and local market trends each influence appraisal outcomes in LA & OC. |

| Preparation improves results | Well-documented upgrades and a well-kept home can help maximize your property’s appraised value. |

| Challenges can be managed | Low appraisals and other roadblocks can often be addressed with the right strategy and expert guidance. |

What is a real estate appraisal and why does it matter?

A real estate appraisal is an independent, professional estimate of a property's market value. A licensed appraiser, who is a neutral third party with no stake in whether the deal closes, conducts the assessment. Their job is to produce an objective report that reflects what the home is actually worth based on current market conditions, not what the buyer hopes to pay or the seller hopes to receive.

Appraisals protect multiple parties at once. For buyers, they confirm you're not overpaying for a property. For lenders, they ensure the loan amount is backed by real collateral. If a borrower defaults, the lender needs to know the property can cover the debt. Without an appraisal, a lender is essentially lending blind. That's why appraisals are standard in nearly all financed home purchases.

Beyond buying and selling, appraisals show up in several other scenarios that many people overlook:

- Mortgage approval: Lenders require an appraisal before funding any home loan to confirm the property's value supports the loan amount.

- Refinancing: When you refinance, your lender orders a new appraisal to reassess current value before adjusting your loan terms.

- Investment purchases: Investors use appraisals to verify that a property's price aligns with its income potential and market position.

For first-time home buyers in Southern California, understanding this process before you make an offer is one of the most powerful moves you can make. Most people don't realize that the appraisal isn't just a formality. It's a financial checkpoint.

According to home appraisal basics from the Consumer Financial Protection Bureau, appraisers must follow strict professional standards and are prohibited from being influenced by any party to the transaction. That independence is what gives the report its authority.

In the Los Angeles and Orange County markets, where a single block can mean a $200,000 difference in value, the appraisal report isn't just paperwork. It's the document that either confirms your deal or forces everyone back to the table.

Understanding what an appraisal is and why lenders require it puts you in a much stronger position, whether you're buying your first home in Anaheim or adding a rental property in Silver Lake.

The appraisal process: Steps, factors, and who's involved

With the importance of appraisals clear, let's look at how the process actually works and which details matter most when your property is in the spotlight.

The lender almost always initiates the appraisal after a purchase agreement is signed. They order it through an appraisal management company, which assigns a licensed appraiser. The appraiser is independent, meaning neither the buyer nor the seller chooses them. Here's how the process typically unfolds:

- Order placed: The lender or appraisal management company assigns a licensed appraiser to the property.

- Property visit: The appraiser schedules an on-site inspection, usually lasting one to three hours depending on the home's size and complexity.

- Data collection: The appraiser measures the home, notes its condition, records features, and photographs every room and exterior.

- Comparable sales analysis: Using recent sales of similar homes nearby, the appraiser builds a value range. Appraisers use a standardized approach focused on recent comparable sales to anchor their final number.

- Report preparation: The appraiser compiles all findings into a formal report, typically using the Uniform Residential Appraisal Report (URAR) form.

- Report delivery: The completed report goes to the lender, who then shares it with the buyer.

For a deeper look at residential appraisal steps, the Appraisal Institute offers detailed guidance on how each phase is conducted.

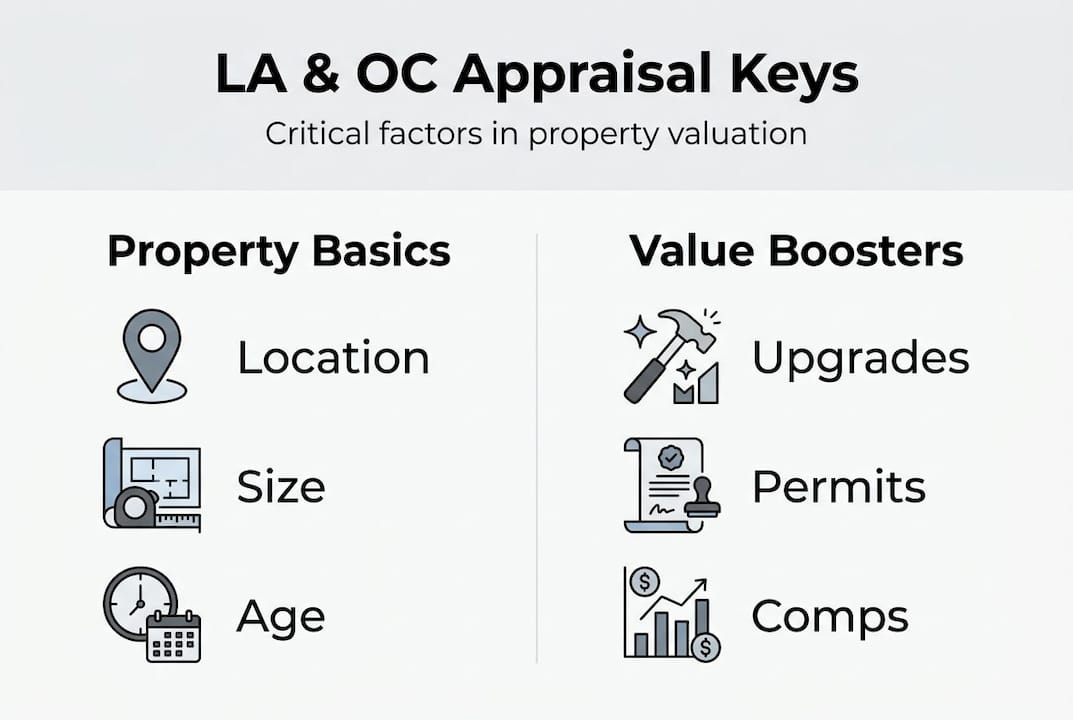

The factors that influence the final value in LA and OC are specific and worth knowing:

| Factor | Typical value impact |

|---|---|

| Location and neighborhood | Very high (can shift value by 20%+) |

| Square footage and lot size | High |

| Recent upgrades and renovations | Moderate to high |

| Property condition | Moderate to high |

| Comparable sales (comps) | Very high |

| Market trends at time of appraisal | Moderate |

| Curb appeal and presentation | Low to moderate |

The biggest surprise for most homeowners is how heavily location and recent comps weigh on the final number. A beautifully renovated kitchen won't save a valuation if nearby sales have been weak.

When listing your home in Los Angeles or Orange County, timing your appraisal around strong comparable sales in your area can make a real difference.

Pro Tip: Before the appraiser arrives, pull recent sales data for similar homes within a half-mile radius. If you find strong comps the appraiser might miss, you can legally provide that information. Appraisers are required to consider relevant data you submit.

Common challenges and how appraisals can kill or save a deal

Understanding the process is only half the battle. Next, it's crucial to know where deals go wrong and how to navigate the pitfalls before they catch you off guard.

Low appraisals remain a major roadblock for buyers and sellers, especially in competitive markets like LA and OC. When a home appraises below the agreed sale price, the lender will only finance up to the appraised value. That gap becomes a problem everyone has to solve.

Several factors commonly push appraisals lower than expected:

- Rapidly shifting markets: If prices have risen sharply since the most recent comparable sales, the appraiser's data may lag behind current conditions.

- Unique or unusual properties: Homes with unconventional layouts, highly custom features, or historic designations are harder to compare to standard sales.

- Deferred maintenance: Visible repairs that haven't been addressed signal risk to appraisers and can reduce value.

- Poor communication: Sellers who don't provide documentation of upgrades or permits leave appraisers working with incomplete information.

Here's a quick comparison of what tends to sink or support an appraisal:

| What hurts an appraisal | What helps an appraisal |

|---|---|

| Unpermitted additions | Documented, permitted upgrades |

| Deferred maintenance | Recent repairs and clean condition |

| Weak or distant comps | Strong nearby comparable sales |

| Overpriced listing vs. market | Realistic pricing aligned to market |

| Missing renovation records | Complete permit and upgrade history |

If you do receive a low appraisal, you have real options. Don't panic. Here's what you can do:

- Request a reconsideration of value: Provide the appraiser with additional comparable sales they may have overlooked.

- Renegotiate the sale price: Ask the seller to lower the price to match the appraised value.

- Cover the gap in cash: Some buyers choose to pay the difference between the appraised value and the sale price out of pocket.

- Walk away: If the contract includes an appraisal contingency, you can exit the deal without penalty.

For those selling property in LA, a proactive approach to documentation and pricing is the best defense against a low appraisal derailing your sale. The market appraisal challenges outlined by the National Association of Realtors confirm that appeals are possible and sometimes successful when backed by solid data.

Pro Tip: Keep a folder with every permit, receipt, and contractor invoice for work done on your home. When the appraiser visits, hand it over. That documentation can directly support a higher valuation.

How to prepare for an appraisal: Maximizing your property's value

Now that you know what can go wrong, you're ready to learn how to influence a successful outcome by preparing your property the right way.

Homes that are clean, well-presented, and repaired often appraise higher. That's not just a suggestion. It reflects how appraisers perceive condition, which directly affects their final number. Preparation is one of the few things you can actually control.

Here's how to organize your home and paperwork for maximum credibility before the appraiser arrives:

- Complete all visible repairs: Fix leaky faucets, patch holes in walls, replace broken fixtures, and address any obvious maintenance issues.

- Deep clean the entire property: A clean home signals that it has been well-maintained. This matters more than most sellers realize.

- Boost curb appeal: Mow the lawn, trim hedges, clear the driveway, and add fresh mulch or flowers if possible.

- Gather all documentation: Compile permits, renovation receipts, HOA documents, and any recent inspection reports.

- Prepare a list of upgrades: Write out every significant improvement with the approximate cost and year it was completed.

- Ensure access to all areas: The appraiser needs to see every room, the attic, the garage, and the exterior. Clear any blocked access points.

For additional guidance on preparing for appraisal, Zillow's seller guide covers practical steps that align well with Southern California market expectations.

In LA and OC's competitive market, even small repairs can shift perception. A cracked tile or a broken window screen might seem minor to you, but to an appraiser, it suggests a pattern of deferred maintenance.

Here are the improvements that most consistently boost appraised value:

- Major: Kitchen remodels, bathroom updates, roof replacement, HVAC upgrades, new windows

- Minor: Fresh interior paint, updated light fixtures, landscaping improvements, refinished hardwood floors, new hardware on cabinets

If you're considering as-is home sales or want to understand how preparation affects your net return, it's worth comparing both paths carefully. And if you're an investor, the investment tips for LA and OC blog covers how appraisal outcomes directly affect your return on investment.

Appraisals in Los Angeles and Orange County: Special considerations

Having mastered the basics and the preparation, let's see what makes appraisals in Los Angeles and Orange County a special challenge compared to the rest of the country.

Southern California's market volatility and diverse neighborhoods can see higher than average appraisal swings compared to more stable markets. A neighborhood in Pasadena can behave completely differently from one in Compton or Newport Beach, even when they're just miles apart.

LA and OC appraisers must account for factors that simply don't exist in most other markets:

- Ocean view premiums: Properties with Pacific Ocean views in cities like Laguna Beach or Malibu carry significant value premiums that are difficult to quantify with standard comps.

- Historic district rules: Homes in designated historic neighborhoods face strict renovation limitations that affect both their appeal and their comparable pool.

- Earthquake retrofitting: California's seismic requirements mean that retrofitted or non-retrofitted homes can appraise differently based on structural compliance.

- HOA fees and restrictions: High monthly HOA fees in condo-heavy markets like Irvine can reduce buyer demand and affect appraised value.

- Luxury feature adjustments: High-end finishes, smart home systems, and resort-style pools require appraisers to find appropriate luxury comps, which are often scarce.

For regional buyer tips specific to navigating these nuances, understanding how local appraisers handle these adjustments gives you a real edge. The appraisals in hot markets analysis from the Wall Street Journal highlights how fast-moving markets like LA create unique pressure on appraisers to keep pace with buyer activity.

Working with a Southern California buyer agent who understands these regional quirks is one of the most underrated advantages a buyer or seller can have going into an appraisal.

A local expert's perspective: What really makes appraisals succeed

Now that we've covered the facts, here's a local perspective on what really matters in the Southern California market.

Online valuation tools like Zestimate or Redfin estimates are useful starting points, but they miss the details that actually move the needle in LA and OC. They can't see that your neighbor's sale was a distressed situation, or that your kitchen was renovated six months ago with premium materials. Relying on those numbers to set expectations before an appraisal is one of the most common and costly mistakes we see.

The buyers and sellers who come out ahead are almost always the ones who treat documentation like a competitive advantage. They have their permits organized, their upgrade history written out, and a clear picture of what comparable sales support their position. That preparation doesn't happen by accident. It happens because they worked with an agent who knows what appraisers actually look for.

Here's the misconception that trips people up most often: the highest offer doesn't guarantee a smooth appraisal. In a bidding war, it's easy to assume the winning price reflects true market value. But appraisers aren't looking at what buyers are willing to pay emotionally. They're looking at what the data supports.

The final appraisal report is also more nuanced than most people realize. The adjustments section, where appraisers add or subtract value for differences between your home and the comps, is where deals quietly get shaped. Most people skip right to the final number. A good agent who knows how to choose the right realtor for your situation will review those adjustments with you and flag anything that looks off.

Get expert appraisal support with INC Realtors

Ready to turn appraisal insight into action? Here's how to get local expert support.

Knowing how appraisals work is valuable. Having an experienced local agent in your corner when one is ordered is even better. At INC Realtors, Irvin Nierras and the team specialize in helping buyers and sellers navigate the Southern California market with confidence, including the appraisal process.

Start with a free home evaluation to get a clear, data-backed picture of what your property is worth right now. You can also check the latest LA/OC market snapshot to understand how current conditions might affect your appraisal outcome. If you're ready to list, our expert selling help connects you with personalized guidance from someone who knows these neighborhoods inside and out. Don't let an appraisal catch you off guard. Get the local knowledge you need before the appraiser walks through the door.

Frequently asked questions

How long does a real estate appraisal take in Los Angeles or Orange County?

Appraisal timing depends on market demand and property type, but most appraisals are completed within 5 to 7 business days in Southern California. Complex or luxury properties may take longer.

What if my home appraises for less than the sale price?

Low appraisals can derail mortgage approvals, but you can contest the value, renegotiate the sale price, or cancel the deal if your contract includes an appraisal contingency. Your lender will not finance above the appraised value.

Do appraisers consider upgrades and renovations when valuing my home?

Yes. Well-documented renovations can positively impact appraised value, especially when you provide permits and receipts that confirm the work was completed properly.

Are appraisals required for cash buyers in California?

Cash buyers can opt out of appraisals since no lender is involved, but many still request one as a safeguard to confirm they're paying a fair price.