TL;DR:

- Appraisals in Southern California can come in above or below the contract price, impacting deals.

- They use recent sales data but face challenges from market speed and unique properties.

- Buyers and sellers should understand and proactively manage the appraisal process to protect their investments.

Most people assume an appraisal is just a hurdle designed to kill a deal. In Southern California's fast-moving 2026 market, that assumption can cost you real money. Appraisals can actually come in above the contract price, creating unexpected leverage for buyers and surprising complications for sellers. Whether you're listing a craftsman bungalow in Pasadena or making an offer on a condo in Irvine, understanding what an appraiser actually does, and why their conclusions matter, is one of the most practical things you can do before you sign anything. This guide walks you through the entire appraisal process, the unique pressures of the Southern California market, and the concrete steps you can take to protect your transaction.

Table of Contents

- What is a home appraiser and why does the role matter?

- How appraisers determine home value: Methods and challenges

- Appraisals in the 2026 Southern California market: What's different?

- What home buyers and sellers need to know: Navigating the appraisal process

- The uncomfortable truth about appraisals in SoCal: What most buyers and sellers miss

- Make confident moves: Find your best home value with expert support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Impartial valuations matter | An appraiser’s unbiased assessment protects both buyers and sellers in a home sale. |

| SoCal markets are unique | Southern California’s fast-moving market can cause appraisal values to differ from sales prices. |

| Know your options | Sellers and buyers should prepare for all appraisal outcomes and understand steps for resolution. |

| Leverage expert guidance | Working with knowledgeable agents and understanding appraisals leads to better home sale decisions. |

What is a home appraiser and why does the role matter?

An appraiser is a licensed professional who gives an independent, unbiased opinion of a property's market value. That independence is the whole point. Unlike a real estate agent, whose income depends on closing a deal, an appraiser has no financial stake in the outcome. Their job is to tell the truth about what a home is worth, even if that truth is inconvenient.

In California, appraisers must be licensed or certified by the Bureau of Real Estate Appraisers (BREA). There are different license levels: Trainee, Licensed Residential, Certified Residential, and Certified General. For most home purchases in Los Angeles and Orange County, you'll encounter a Certified Residential appraiser, who is qualified to appraise any one-to-four unit residential property regardless of value.

Here's how the process typically works in a standard purchase transaction:

- The buyer's lender orders the appraisal after the purchase agreement is signed

- The buyer pays the appraisal fee upfront, which typically runs $300 to $700 and takes one to two weeks to complete

- The appraiser conducts a physical inspection of the property

- They research recent comparable sales and market data

- They produce a written report with a final value opinion

- The lender uses that value to determine how much they'll lend

The appraiser's report protects everyone involved. The lender doesn't want to loan $900,000 on a home worth $750,000. The buyer doesn't want to overpay. Even the seller benefits from an objective benchmark that validates their asking price.

For a deeper look at how this fits into the broader purchase process, the real estate appraisal basics guide covers the full picture for LA and OC buyers.

California also enforces strict appraiser independence rules under federal law (the Dodd-Frank Act). Lenders cannot pressure appraisers to hit a specific number. Appraisers must be selected through an Appraisal Management Company (AMC) or through a firewall process that prevents loan officers from influencing the choice.

"An appraiser's value opinion is not a negotiating position. It is a professional conclusion based on evidence, and it carries legal weight in the transaction."

This independence is exactly why appraisals sometimes create friction. When a seller prices a home based on emotion or a hot weekend of open houses, and the appraiser's data tells a different story, conflict is almost inevitable. Knowing this ahead of time puts you in a much stronger position.

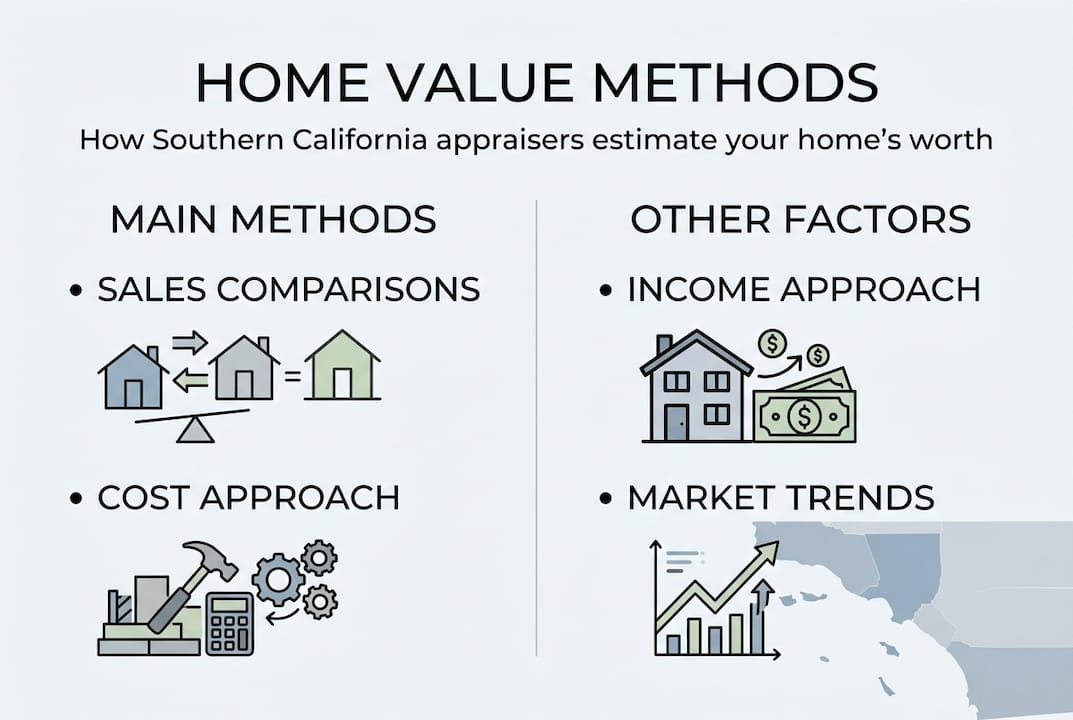

How appraisers determine home value: Methods and challenges

With the basic role defined, it's important to understand exactly how an appraiser arrives at a home's value, and why that value might surprise you in SoCal.

For residential properties, the primary tool is the sales comparison approach. Appraisers analyze recent comparable sales from the past three to six months, then make dollar adjustments for differences between those sales and the subject property. This is sometimes called "comps" analysis.

Here's what appraisers typically adjust for:

| Feature | Typical Adjustment Direction |

|---|---|

| Gross living area (square footage) | + or per sq ft |

| Bedroom/bathroom count | + or based on market |

| Lot size | + or especially in SoCal |

| Condition and updates | + for remodels, for deferred maintenance |

| Location (view, proximity) | + or based on desirability |

| Garage or parking | + in urban LA/OC |

The process sounds mechanical, but it requires real judgment. Two homes on the same street can have very different values based on a kitchen remodel, a hillside view, or a noisy freeway behind the fence.

Southern California creates several unique complications:

- Fast price movement: When prices rise quickly, recent comps may not reflect today's market. Appraisers are constrained by data that is already 30 to 180 days old.

- Unique properties: Mid-century modern homes in Palm Springs, hillside properties in Silver Lake, or custom builds in Newport Beach often have very few true comparables.

- Hyper-local variation: A half-mile difference in Los Angeles can mean a $200,000 swing in value. Appraisers unfamiliar with the micro-market may miss this.

- Competitive bidding: When buyers bid 15% over asking, the contract price reflects buyer emotion, not necessarily market value. Low appraisals are more common in SoCal precisely because of this dynamic.

Pro Tip: If you're selling a unique property, gather your own list of the three to five most similar recent sales before the appraisal. You can give this to your agent, who can legally share it with the appraiser as supplemental information. This won't change the appraiser's independence, but it can ensure they don't miss a key comp.

Appraisals can also come in above the contract price. This happens most often with unique homes that have few comps, or in areas where sellers may have underpriced. When that occurs, the buyer is essentially getting instant equity. It's a less-discussed outcome, but it matters a lot for buyers thinking about investing in SoCal real estate for long-term wealth.

Appraisers also consider the cost approach (what it would cost to rebuild the home) and the income approach (relevant for multi-unit properties), but for single-family homes in LA and OC, the sales comparison approach carries the most weight.

Appraisals in the 2026 Southern California market: What's different?

Now that you know how appraisers work and SoCal's quirks, it's time to dig into what's actually happening in this year's local market.

The 2026 SoCal market is defined by a painful tension: prices remain elevated, but buyer demand has cooled sharply. SoCal sales ran 31% below average in early 2026, driven by monthly payments that have surged 59% over the past four years. That combination creates a tricky environment for appraisals.

Key 2026 market data for SoCal appraisals:

| Metric | 2026 SoCal Snapshot |

|---|---|

| Monthly payment increase (4-year) | Up 59% |

| Sales volume vs. historical average | Down ~31% |

| Low appraisal rate vs. national avg | Higher than 10% national rate |

| Typical appraisal cost | $300 to $700 |

When sales volume drops, appraisers have fewer recent comps to work with. That forces them to reach back further in time or expand their geographic search area, both of which reduce precision. In a market where prices shifted significantly over the past year, a comp from eight months ago may not reflect today's reality at all.

Stat to know: In hot SoCal markets like Los Angeles, the rate of appraisals coming in below contract price exceeds the 10% national average, creating real risk for financed buyers.

Here's what this means practically for buyers and sellers:

- Sellers who price aggressively may face an appraisal gap, where the buyer's lender won't fund the full purchase price

- Buyers in bidding wars may need to bring extra cash to cover the gap between appraised value and contract price

- Cash buyers sidestep the appraisal entirely, which is one reason cash offers are so powerful in SoCal right now

- Closing timelines can stretch when an appraisal comes in low and parties need to renegotiate

For sellers, the silver lining is that lower sales volume also means fewer competing listings. If your home is priced correctly and shows well, a strong appraisal can actually accelerate your sale by removing financing uncertainty early. Knowing the prime SoCal investment spots can also help you understand which neighborhoods are most likely to produce clean appraisals right now.

The bottom line: in 2026, the appraisal isn't just a formality. It's a real variable that can determine whether your deal closes, how quickly it closes, and at what final price.

What home buyers and sellers need to know: Navigating the appraisal process

With the stakes so high in Southern California, understanding how to handle the appraisal process is crucial. Here's how to turn insight into action.

For sellers: Prepare before the appraiser arrives

- Clean and declutter every room. Appraisers assess condition, and a clean home signals good maintenance. First impressions matter even for professionals.

- Complete minor repairs. Fix leaky faucets, patch holes in walls, and replace broken fixtures. Deferred maintenance triggers downward adjustments.

- Document all upgrades. Prepare a written list of improvements with dates and approximate costs. A new roof, updated HVAC, or remodeled kitchen all add value, but only if the appraiser knows about them.

- Research your own comps. Look at what similar homes sold for in the past three to six months within a one-mile radius. Share this with your agent.

- Be present but not intrusive. You can answer factual questions, but don't follow the appraiser room to room or try to influence their opinion.

For buyers: Know your options when the appraisal comes in low

The appraisal process takes one to two weeks and costs $300 to $700, so plan for this in your timeline and budget. If the appraisal comes in below the contract price, you have several options:

- Request a rebuttal (reconsideration of value). Your agent can submit comparable sales the appraiser may have missed. This is formal and must go through the lender.

- Renegotiate the price. Ask the seller to reduce the price to the appraised value. In a slower market, many sellers will agree.

- Cover the gap in cash. If you have the funds and want the home, you can pay the difference between the appraised value and the contract price out of pocket.

- Walk away. If your contract includes an appraisal contingency (and it should), a low appraisal lets you exit without losing your deposit.

Pro Tip: Always include an appraisal contingency in your offer unless you are paying cash and have done your own independent valuation. Waiving this contingency is a major risk in any market.

Knowing the right key agent questions to ask before hiring representation can also help you find someone who knows how to handle appraisal disputes effectively. And if you're new to the process, working with a buyer's agent who understands local appraisal patterns is one of the smartest moves you can make. You can also get a free home value report to benchmark your property before the appraiser even shows up.

The uncomfortable truth about appraisals in SoCal: What most buyers and sellers miss

Here's what years of working in this market have made clear: most buyers and sellers treat the appraisal as the final word on value. That's a mistake.

An appraisal is a snapshot, not a verdict. It reflects one appraiser's interpretation of limited data at a specific point in time. In a market as dynamic and geographically complex as Southern California, that snapshot can be genuinely wrong in either direction. Appraisals can exceed the contract price in areas with thin comps or unique properties, meaning buyers sometimes get a better deal than they realize, and sellers sometimes leave money on the table.

The real danger is when people make major financial decisions based entirely on the appraised number without understanding its limitations. A seller who drops their price to match a low appraisal without challenging it may be giving away equity. A buyer who walks away because an appraisal came in slightly low may be missing a property that will appreciate significantly.

Market knowledge, not just appraisal data, is what separates good real estate decisions from costly ones. An agent who knows that a specific block in Culver City has been appreciating 8% annually, or that a new transit line is about to open near a listing in Anaheim, brings context that no appraisal report can capture. That's why working with a local agent who genuinely understands the neighborhood is not just convenient. It's a financial advantage.

Use the appraisal as one input among several. Combine it with current listing data, neighborhood trends, and expert guidance to make decisions you'll feel confident about long after closing day.

Make confident moves: Find your best home value with expert support

Armed with this knowledge, you're ready to take effective action in the SoCal market.

Understanding appraisals is only the beginning. Knowing how to act on that understanding is what actually protects your investment. Whether you're a seller trying to price your home accurately or a buyer navigating a competitive offer situation, having the right support makes all the difference in a market this complex.

Irvin Nierras and the team at IN Realtors specialize in residential transactions across Los Angeles and Orange County. You can request a free home evaluation to get a data-driven baseline before your appraisal. If you're ready to buy, search available homes with current listings across SoCal. Sellers can access personalized pricing strategy and full transaction support by visiting get selling support. Real clarity, real expertise, real results.

Frequently asked questions

How long does a home appraisal take in Southern California?

The appraisal process usually takes one to two weeks in Southern California, from the time the lender orders it to when the report is delivered.

Who pays for the home appraisal when selling a house?

The home buyer typically pays the appraisal fee, which ranges from $300 to $700 in Southern California, usually collected upfront before the inspection.

Why do some appraisals come in low in Southern California?

Low appraisals are more common in SoCal because competitive bidding often pushes contract prices above what recent comparable sales can support.

Can an appraisal be higher than the purchase price?

Yes, appraisals can exceed the contract price, particularly in neighborhoods with few comparable sales or highly unique properties where the appraiser finds strong supporting data.

What should I do if my appraisal is lower than expected?

Talk to your agent immediately about requesting a formal reconsideration of value, renegotiating the purchase price with the seller, or deciding whether covering the gap in cash makes financial sense for your situation.