If you're buying or investing in Southern California real estate, you've probably heard the term closing agent tossed around during escrow discussions. Yet many buyers remain unclear about who this person is, what they actually do, and why their role matters so much. In Southern California residential property transactions, the closing agent is typically a licensed Escrow Officer from an independent escrow company acting as a neutral fiduciary for all parties. Understanding their responsibilities, fees, and how they prevent costly delays empowers you to navigate closings with confidence and avoid surprises that derail deals.

Table of Contents

- Key takeaways

- Who is the closing agent and why are they essential in Southern California?

- Core responsibilities and tasks handled by closing agents

- Closing costs and fee structure unique to Southern California

- Common challenges and risk mitigation handled by closing agents

- How homebuyers and investors can best work with closing agents

- Summary: the indispensable role of closing agents in Southern California real estate

- Explore Southern California homes with expert guidance

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Neutral fiduciary role | They serve as neutral fiduciaries who manage escrow tasks and keep negotiations fair for buyers, sellers, and lenders. |

| Title searches and funds | They order title searches, handle earnest money, and disburse funds only after all conditions are met. |

| Fees and differences | Fees are typically split between buyer and seller, with regional variations. |

| Prevent delays and disputes | Proactive closing agents help prevent transaction failures and disputes by verifying conditions and coordinating with all parties. |

Who is the closing agent and why are they essential in Southern California?

In Southern California residential property transactions, the closing agent is typically a licensed Escrow Officer from an independent escrow company acting as a neutral fiduciary for all parties. Unlike some states where attorneys handle closings, California relies heavily on independent escrow companies to ensure neutrality in transactions where conflicts of interest could arise. This independence becomes critical when buyer and seller interests diverge or when lenders impose strict funding conditions.

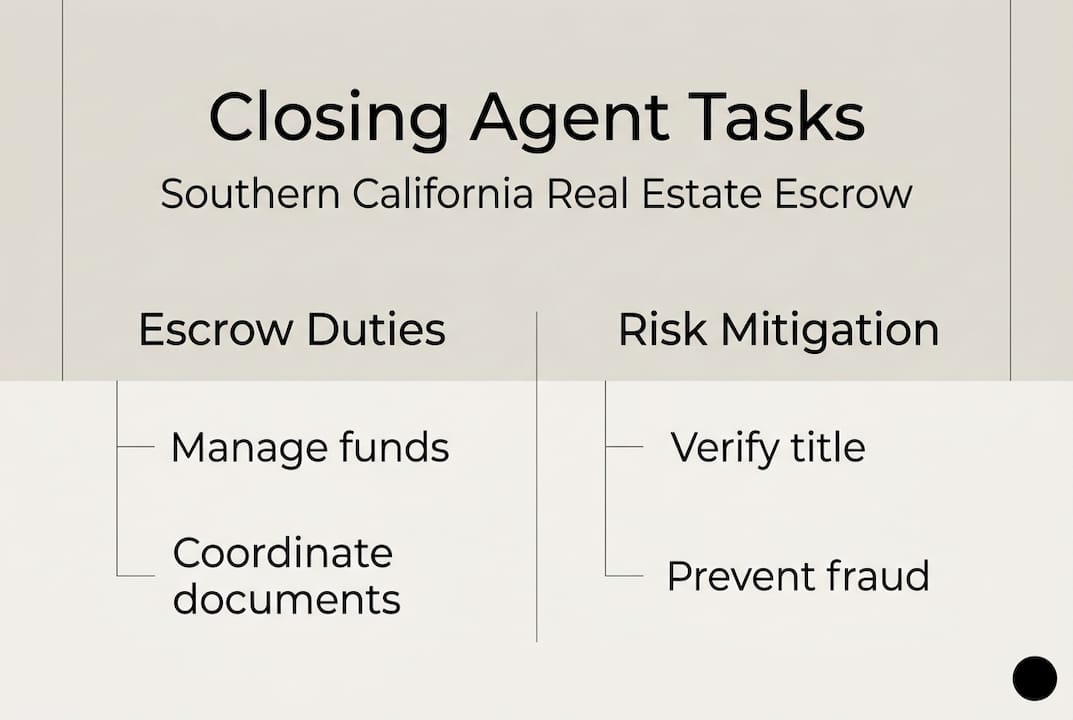

The closing agent's fiduciary duties require acting impartially for buyer, seller, and lender simultaneously. They cannot favor one party over another or provide legal advice that benefits a single stakeholder. This neutrality protects all parties from premature fund releases, incomplete documentation, or contract violations that could trigger litigation. Their role encompasses handling all escrow instructions, managing funds in segregated accounts, and coordinating with title companies, lenders, and real estate agents to satisfy every condition before closing.

Pro Tip: Understanding the closing agent's strict independence helps you recognize why they cannot expedite processes or bend rules, even when delays frustrate you. Their neutrality is your protection against costly mistakes.

Key responsibilities include:

- Managing all escrow instructions and ensuring compliance with contract terms

- Holding and safeguarding earnest money deposits and closing funds

- Coordinating with title companies, lenders, inspectors, and agents

- Verifying all conditions are met before releasing funds or recording deeds

- Maintaining detailed records for regulatory compliance and dispute resolution

When evaluating properties, having accurate home value evaluation data helps you understand whether the purchase price aligns with market conditions, which the closing agent will verify through title and appraisal coordination.

Core responsibilities and tasks handled by closing agents

Closing agents perform a complex sequence of tasks during escrow, each critical to preventing delays or legal disputes. Core mechanics include ordering title searches and payoff statements, preparing Closing Disclosure ensuring CFPB compliance, managing segregated escrow accounts, prorating costs, verifying signatures and conditions, recording deeds, and disbursing funds only after all instructions are met. The Consumer Financial Protection Bureau requires lenders to provide the Closing Disclosure at least three business days before closing, and closing agents ensure this timeline is strictly followed.

Managing funds in segregated escrow accounts protects buyers and sellers from fraud or misappropriation. The closing agent calculates prorations for property taxes, HOA fees, utilities, and insurance, ensuring each party pays their fair share based on the closing date. This precision prevents post-closing disputes over who owes what.

Pro Tip: Request your Closing Disclosure as soon as it's available and review every line item carefully. Catching errors early prevents last-minute closing delays or unexpected out-of-pocket costs.

The typical closing process follows these steps:

- Open escrow and deposit earnest money into segregated account

- Order preliminary title report and identify any liens or encumbrances

- Coordinate inspections, appraisals, and lender underwriting requirements

- Prepare and distribute Closing Disclosure meeting CFPB timelines

- Verify all contingencies removed and conditions satisfied per contract

- Collect final funds from buyer and lender, confirm amounts match CD

- Record deed and related documents with county recorder's office

- Disburse funds to seller, pay off existing liens, and distribute remaining proceeds

| Task | Timeline | Party responsible |

|---|---|---|

| Earnest money deposit | Within 3 days of acceptance | Buyer |

| Title search ordered | Within 2 days of opening escrow | Closing agent |

| Closing Disclosure delivery | 3 business days before closing | Lender/Closing agent |

| Final walkthrough | 1 day before closing | Buyer |

| Deed recording | Day of closing | Closing agent |

Accurate property valuation reports support the appraisal process, which closing agents coordinate to ensure lender funding conditions are met on schedule.

Closing costs and fee structure unique to Southern California

In SoCal, escrow fees benchmark around $2 per $1,000 purchase price plus $250 base, resulting in approximately $2,050 on a $900,000 home, split 50/50 between buyer and seller. This differs significantly from Northern California, where buyers often shoulder more of the escrow costs. The seller traditionally pays for owner's title insurance in Southern California, while buyers pay for lender's title insurance, creating a more balanced cost distribution.

Understanding this fee structure helps you budget accurately and avoid surprises at closing. Escrow fees cover the closing agent's services, including document preparation, notary services, wire transfers, recording fees, and administrative overhead. Additional costs like title insurance, transfer taxes, and recording fees appear as separate line items on your Closing Disclosure.

Typical cost breakdown for a $900,000 Southern California home:

- Escrow fee: $2,050 total ($1,025 buyer, $1,025 seller)

- Owner's title insurance: $3,500 (seller pays)

- Lender's title insurance: $1,200 (buyer pays)

- County transfer tax: $990 (typically seller pays)

- City transfer tax: varies by municipality (usually seller pays)

- Recording fees: $150 (split or buyer pays)

- Notary and courier: $100 (included in escrow fee)

| Cost component | Southern California | Northern California |

|---|---|---|

| Escrow fee split | 50/50 buyer/seller | Often 60/40 or 70/30 favoring seller |

| Owner's title insurance | Seller pays | Buyer pays |

| Lender's title insurance | Buyer pays | Buyer pays |

| Transfer tax | Seller pays | Seller pays |

Knowing your home's worth evaluation before making an offer helps you calculate total closing costs as a percentage of purchase price, typically ranging from 2% to 3% for buyers in Southern California.

Common challenges and risk mitigation handled by closing agents

Edge cases include title defects or liens delaying clearance, financing or appraisal issues, inspection repair disputes, unmet contingencies, and escrow errors in instructions leading to delays or litigation. Remedies include mediation, specific performance claims, or damages up to 3% of purchase price as liquidated damages in standard California contracts. Closing agents remain vigilant to identify these risks early and coordinate solutions while maintaining strict neutrality.

Title defects such as unreleased liens, boundary disputes, or undisclosed easements can halt closings until resolved. The closing agent works with title companies to clear these issues, but complex cases may require legal intervention or seller concessions. Financing delays occur when lenders discover last-minute credit issues, employment changes, or appraisal shortfalls that violate underwriting guidelines.

Closing agents cannot provide legal advice due to their strict neutrality obligation. If you face a dispute over inspection repairs or contract interpretation, consult a qualified real estate attorney rather than relying on the closing agent for guidance. Their role is to enforce the contract as written, not to advocate for your position or negotiate terms.

"Closing agents uphold fiduciary duties to all parties equally, protecting buyers from premature fund releases and sellers from contract violations. Courts consistently enforce this neutrality, making the closing agent's impartiality a cornerstone of California real estate law."

Common obstacles that delay or derail closings:

- Undisclosed liens or judgments discovered during title search

- Appraisal coming in below purchase price, requiring renegotiation

- Buyer's financing falling through due to credit or employment changes

- Seller failing to complete agreed-upon repairs before final walkthrough

- Missing signatures or incorrectly executed documents requiring re-signing

- Wire fraud attempts targeting closing funds through email phishing

Modern closing agents use tools like SAFEvalidation to prevent wire fraud by verifying wire instructions through secure channels. Always confirm wire details by phone using a verified number, never by email alone. Having an accurate property evaluation report reduces appraisal risk by ensuring your offer aligns with market value.

How homebuyers and investors can best work with closing agents

Closing agents mitigate risks for homebuyers and investors by enforcing contract terms impartially and preventing premature fund release. In SoCal's custom, cost splits favor buyers on title insurance compared to other regions. Understanding how to collaborate effectively with your closing agent ensures smooth closings and minimizes surprises.

Start by reviewing your Closing Disclosure immediately upon receipt, at least three business days before closing. Compare every line item against your good faith estimate and loan estimate to catch discrepancies early. Question any fees that seem inflated or unexpected, and request explanations in writing if needed.

Pro Tip: Confirm escrow instructions and contingency deadlines in writing as soon as escrow opens. Missing a deadline by even one day can give the other party grounds to cancel the contract or claim damages.

Steps to prepare and stay ahead during escrow:

- Respond promptly to all closing agent requests for documents or information

- Review preliminary title report within 48 hours and raise any concerns immediately

- Schedule final walkthrough 24 hours before closing to verify property condition

- Arrange wire transfer or cashier's check for closing funds at least 2 days early

- Verify wire instructions by phone using a number you look up independently

- Keep all parties informed of any changes to employment, credit, or finances

- Attend closing with valid government-issued photo ID and all required documents

Maintain clear communication and respond promptly to agent requests. Delays in providing pay stubs, bank statements, or signed documents can push back closing dates and trigger rate lock expirations or contract penalties. Treat every deadline as firm and non-negotiable unless you obtain written extensions from all parties.

Leverage home value estimation tools early in your search to make competitive offers that appraise smoothly, reducing one major source of closing delays and renegotiations.

Summary: the indispensable role of closing agents in Southern California real estate

Closing agents ensure safe, compliant, and neutral transaction closings by managing complex documentation, funds, and regulatory requirements. They protect buyers, sellers, and lenders equally by enforcing contract terms without favoritism or bias. Understanding fees and charges helps buyers and sellers prepare accurate budgets and avoid last-minute cash shortfalls. Proactive cooperation with agents reduces risk of delays or disputes that can derail deals or trigger litigation.

Key insights to remember:

- Closing agents act as neutral fiduciaries, not advocates for any single party

- Southern California's 50/50 escrow fee split differs from Northern California customs

- Early review of Closing Disclosure and title reports prevents costly surprises

- Common challenges like title defects and financing delays require patience and flexibility

- Your closing agent cannot provide legal advice, so consult attorneys when needed

Knowledge empowers confident decision making in Southern California markets. Understanding the closing agent's role, limitations, and fee structure positions you to navigate escrow smoothly and close deals successfully. Whether you're a first-time homebuyer or seasoned investor, respecting the closing process and working collaboratively with your escrow officer protects your interests and ensures a positive transaction experience.

Explore Southern California homes with expert guidance

Now that you understand how closing agents protect your interests during escrow, take the next step toward successful homeownership or investment in Southern California. Access comprehensive homes for sale listings tailored to Los Angeles and Orange County markets, backed by current Southern California market snapshot data that informs smarter offers. Utilize professional home value reports to ensure your purchase price aligns with true market value before entering escrow.

Irvin Nierras at HomeSmart Evergreen brings deep local expertise and personalized service to guide you through every step of the buying process. From initial property search through final closing, having an experienced agent who understands Southern California's unique escrow customs and closing agent requirements makes all the difference in achieving a smooth, successful transaction.

FAQ

What is the role of a closing agent in real estate transactions?

Closing agents act as neutral third parties managing documents and funds to finalize real estate deals. They protect interests of buyer, seller, and lender by enforcing contract terms impartially. Their responsibilities include ordering title searches, preparing closing documents, managing escrow accounts, and ensuring all conditions are met before recording deeds and disbursing funds.

How are escrow fees typically split between buyers and sellers in Southern California?

SoCal usually splits escrow fees 50/50 between buyer and seller, with each party paying approximately half of the total cost. Sellers traditionally pay for owner's title insurance, unlike in Northern California where buyers often cover this expense. This regional custom creates a more balanced cost distribution compared to other California markets.

What common issues can cause delays in escrow closings?

Title issues, liens, and appraisal or financing problems cause most delays in Southern California closings. Unmet contingencies, inspection negotiations, or errors in escrow instructions also contribute to timeline extensions. Closing agents work to resolve or mitigate these issues promptly, but complex title defects or lender underwriting problems may require legal intervention or contract renegotiation.

Can closing agents provide legal advice during the escrow process?

Closing agents must remain neutral and cannot provide legal advice to any party in the transaction. Buyers and sellers should consult qualified real estate attorneys for legal questions about contract interpretation, dispute resolution, or rights and obligations. The closing agent's role is to enforce the contract as written, not to advocate for any party's interests or provide legal counsel.