TL;DR:

- Property appraisal is a licensed assessment that determines a property's market value using standardized methods. It protects lenders and helps buyers avoid overpaying, while the process involves a property visit, research, and a written report. Buyers should understand appraisal options and review reports early to handle potential low values effectively.

Property appraisal is a formal, expert assessment that determines a property's fair market value using standardized valuation methods and real market evidence. The industry term is real estate appraisal, and it sits at the center of nearly every home purchase, refinance, and mortgage decision. Appraisers follow standards set by USPAP (Uniform Standards of Professional Appraisal Practice), the nationally recognized code governing licensed appraisers in the United States. Understanding what is property appraisal means, how it works, and what it can cost you is the single most practical thing a first-time homebuyer can do before signing a purchase contract.

What is property appraisal and why does it matter?

A property appraisal is a formal opinion of value prepared by a qualified appraiser based on recognized valuation methods and market evidence. It is not a guess, and it is not the same as the price you agreed to pay. The appraiser produces a written report that a lender uses to decide how much money to loan against the property.

The importance of property appraisal goes beyond satisfying a lender's checklist. Appraisals protect buyers from overpaying for a home by anchoring the transaction to objective market data. They also protect sellers from pricing a home so far above market value that financing falls apart at the last minute.

Appraisal is distinct from two concepts that first-time buyers often confuse it with. A home inspection evaluates the physical condition of the property, looking for structural defects, roof damage, or plumbing issues. An appraisal evaluates market value, not physical defects. Assessed value, set by a local tax authority, is a separate figure used only to calculate property taxes and rarely matches appraised or market value.

Appraisals primarily serve to protect lenders by confirming the collateral is worth the loan amount. Buyers who understand this avoid the common mistake of treating the appraisal as a personal endorsement of their purchase decision.

How does the property appraisal process work?

The appraisal process follows a clear sequence. Knowing each step removes the anxiety that catches most first-time buyers off guard.

- The lender orders the appraisal. After you go under contract, your mortgage lender hires a licensed appraiser, usually through an appraisal management company. You do not choose the appraiser.

- You pay the appraisal fee upfront. A standard appraisal costs around $500 for a single-family home, paid out of pocket by the buyer. This fee is non-refundable even if the deal falls through.

- The appraiser schedules a property visit. The appraiser walks through the home, measures square footage, notes the condition of rooms, and photographs key features. The visit typically takes one to three hours.

- The appraiser researches comparable sales. After the visit, the appraiser pulls recent sales of similar homes in the area, called comparables or "comps," and adjusts for differences in size, condition, and features.

- The report is delivered to the lender. Appraisal reports typically take 7–10 days from assignment to delivery. The lender then shares the report with you before closing.

Appraisers weigh several factors when forming their value opinion. Location, school districts, condition, amenities, and recent sales trends all influence the final number. A home in a top-rated school district in Orange County will appraise differently than a structurally identical home in a lower-demand area, even if the asking prices are similar.

Pro Tip: Request a copy of the appraisal report as soon as the lender receives it. You have a legal right to see it, and reviewing it early gives you time to flag errors before closing.

What are the main methods used to appraise property value?

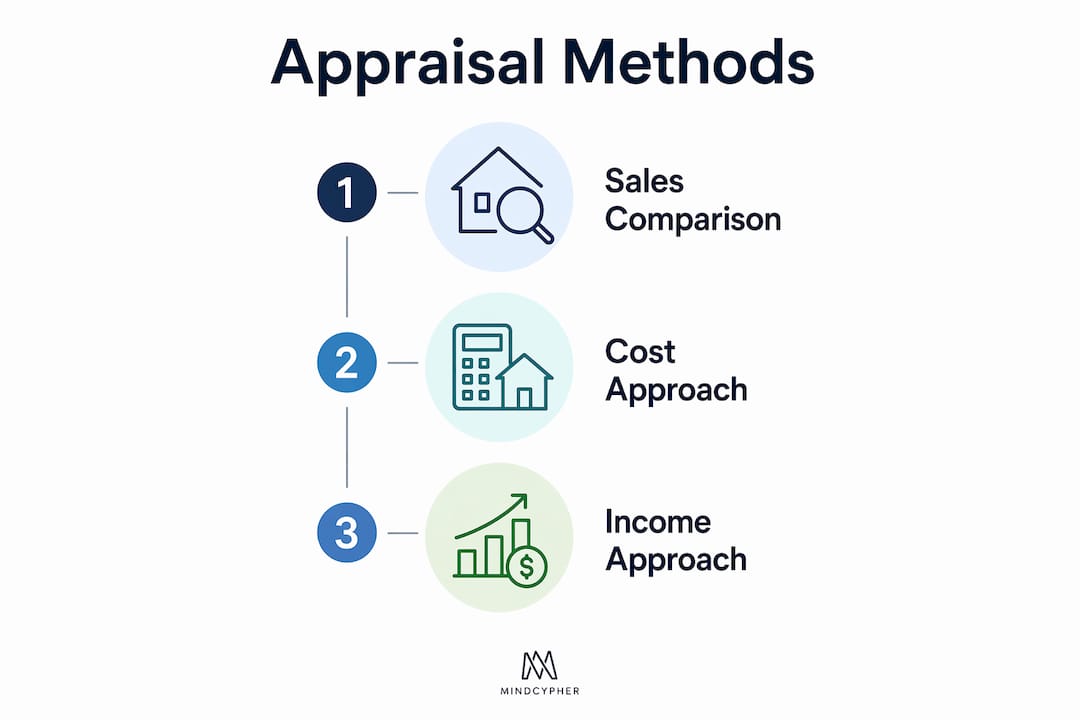

Appraisers use three primary approaches to determine value. The choice of method depends on the property type and the available market data.

Sales comparison approach

The sales comparison approach is the standard method for residential homes. The appraiser identifies three to five recently sold properties that closely match the subject property in size, location, age, and condition. Each comparable sale is then adjusted up or down to account for differences. If a comp has an extra bathroom that the subject property lacks, the appraiser subtracts value from that comp. The adjusted values are then reconciled into a single opinion of value.

This method works well in active markets where recent sales data is plentiful. In Southern California markets like Los Angeles and Orange County, where Increaltors operates, comparable sales are usually available within a short radius and a recent time window, making this approach reliable.

Cost approach

The cost approach calculates value by adding the estimated land value to the cost of rebuilding the structure from scratch, then subtracting depreciation for age and wear. This method is most useful for new construction, unique properties, or homes in areas with few comparable sales. It is rarely the primary method for standard residential transactions, but appraisers use it as a cross-check.

Income approach

The income approach applies primarily to rental properties and investment real estate. The appraiser estimates the income the property could generate, then converts that income stream into a value using a capitalization rate. For a standard owner-occupied home purchase, this approach is generally not the primary method. If you are buying a duplex or small multi-unit property, expect the appraiser to apply it alongside the sales comparison approach.

Appraisers select comparables and apply adjustments using expert judgment, not a mechanical formula. Two appraisers reviewing the same property can reach slightly different values, which is why the appraiser's qualifications and local market knowledge matter.

Pro Tip: Ask your real estate agent to pull the same comps the appraiser is likely to use before the appraisal visit. If you spot a strong recent sale nearby that supports your purchase price, share it with the appraiser. Appraisers are required to consider relevant data you provide.

| Approach | Best used for | Key inputs |

|---|---|---|

| Sales comparison | Owner-occupied homes | Recent comparable sales, adjustments |

| Cost approach | New builds, unique properties | Land value, rebuild cost, depreciation |

| Income approach | Rental and investment properties | Rental income, capitalization rate |

How do appraisal results impact homebuyers and sellers?

The appraisal result shapes what happens next in your transaction. A value that meets or exceeds the purchase price clears the path to closing. A value that comes in below the purchase price creates what the industry calls an appraisal gap, and that gap requires a decision.

When a low appraisal affects the transaction, buyers typically have four options:

- Renegotiate the purchase price. Ask the seller to lower the price to match the appraised value. In a buyer's market, sellers often agree. In a competitive market like Southern California, they may not.

- Pay the difference in cash. If you have the funds, you can cover the gap between the appraised value and the purchase price out of pocket. The lender will only loan based on the appraised value.

- Request a reconsideration of value. Submit additional comparable sales to the appraiser and ask them to review their conclusion. This works when you have strong data the appraiser may have missed.

- Order a second appraisal. In some cases, you can request a new appraisal, though this adds cost and time and is not guaranteed to produce a higher value.

Maintaining property condition directly affects appraised values by reflecting the home's utility and desirability compared to comparable properties. Sellers who want to protect their asking price should address deferred maintenance, clean up the exterior, and fix obvious defects before the appraiser arrives. Fresh paint, working fixtures, and a clean yard cost little but signal a well-maintained home.

The appraised value and the purchase price are separate numbers. The lender uses the lower of the two to calculate your loan amount. If you agreed to pay $750,000 for a home that appraises at $720,000, your lender bases the loan on $720,000. You are responsible for covering the $30,000 gap in addition to your down payment.

The appraised value also differs from the tax-assessed value on your property tax bill. Tax assessments use their own methodology, often lag behind the market, and serve a different purpose entirely. Do not use your property tax bill to estimate what a home will appraise for.

Common misconceptions about property appraisal

First-time buyers carry a lot of assumptions into the appraisal process. Most of those assumptions create unnecessary stress. Clearing them up early makes the entire transaction smoother.

- "The appraisal confirms the home is in good shape." It does not. Appraisal differs from home inspection in a fundamental way: the appraiser assesses market value, not physical condition. A home can appraise at full value and still have a failing HVAC system or a leaky roof. Always get a separate home inspection.

- "The appraised value is the true market price." The appraisal is a professional opinion, not a guarantee. Appraisals are objective but involve appraiser judgment, and two qualified appraisers can reach different conclusions on the same property. Market conditions, buyer demand, and negotiation all play roles that an appraisal cannot fully capture.

- "A high appraisal means I got a great deal." An appraisal above the purchase price is good news for your financing, but it does not mean the home is underpriced. It means the appraiser found market support for a value at or above what you agreed to pay.

- "I can influence the appraisal by being friendly." Appraisers follow USPAP standards and are legally required to be independent. Attempting to pressure or influence an appraiser is a federal offense under the Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA).

- "If I disagree with the appraisal, there is nothing I can do." Borrowers have the right to review the appraisal report before closing. If you find factual errors, such as the wrong square footage or missing rooms, you can formally request a correction.

Pro Tip: Read the appraisal report carefully and check the comparables the appraiser used. If a comp is in a clearly inferior location or sold under distressed conditions, that is worth raising with your lender.

Valuation is rigorous and evidence-based, providing an objective market-supported value that is distinct from negotiated prices or emotional considerations. That rigor is what makes the appraisal useful. It is also what makes it feel impersonal when the number does not match your expectations.

Key takeaways

A property appraisal is a lender-required, USPAP-governed opinion of market value that directly controls how much a mortgage lender will loan on a home purchase.

| Point | Details |

|---|---|

| Appraisal vs. inspection | An appraisal measures market value; a home inspection evaluates physical condition. They are separate processes. |

| Standard cost and timeline | Expect to pay around $500 and wait 7–10 days for the completed appraisal report. |

| Three valuation methods | Appraisers use sales comparison, cost, and income approaches; sales comparison is standard for homes. |

| Low appraisal options | Buyers can renegotiate, pay the gap, request reconsideration, or order a second appraisal. |

| Borrower review rights | You have the right to review the appraisal report before closing and flag factual errors. |

What I have learned from watching buyers navigate appraisals

Working with buyers across Los Angeles and Orange County, I have seen appraisals derail deals that should have closed easily. Almost every time, the problem was not the appraisal itself. It was that the buyer had no idea what the appraisal was actually measuring.

The biggest mistake I see is buyers treating the appraisal as a formality. They assume it will come in fine, and when it does not, they panic. A low appraisal is not a disaster. It is a data point. The buyers who handle it well are the ones who already know their options before the report arrives.

I also tell every buyer to get a home value estimate before making an offer. Not because it replaces the appraisal, but because it gives you a realistic anchor. If your offer is significantly above what the market data supports, you should know that before you are under contract and paying a $500 appraisal fee.

One more thing: the appraiser works for the lender, not for you. That is not a conflict of interest. It is just the structure of the process. Understanding that distinction helps buyers stop expecting the appraisal to validate their emotional attachment to a home. The appraiser is answering one question: what would a typical buyer pay for this property in this market right now? Your job is to make sure the answer supports your deal.

— Irvin Nierras

Homes and appraisal guidance available through Increaltors

Increaltors serves buyers across Los Angeles, Orange County, and surrounding Southern California communities with current listings and real market knowledge.

Whether you are searching for single-family homes for sale or exploring condos and other property types, Increaltors provides listings paired with the local insight you need to understand what a property is actually worth before you make an offer. Agent Irvin Nierras works directly with buyers to prepare them for the appraisal process, interpret results, and protect their interests through closing. Reach out to Increaltors for personalized guidance on your next purchase in Southern California.

FAQ

What is the property appraisal meaning in simple terms?

A property appraisal is a licensed appraiser's written opinion of a home's fair market value, based on comparable sales and recognized valuation methods. Lenders require it before approving a mortgage.

How long does a property appraisal take?

The appraisal process typically takes 7–10 days from the time the appraiser is assigned to when the completed report is delivered to the lender.

Who pays for the appraisal?

The buyer pays the appraisal fee, which averages around $500 for a single-family home, even though the lender orders the appraisal.

What happens if the appraisal comes in lower than the purchase price?

A low appraisal means the lender will only loan based on the appraised value. Buyers can renegotiate the price, pay the difference in cash, request a reconsideration of value, or order a second appraisal.

Is a property appraisal the same as a home inspection?

No. An appraisal determines market value for the lender. A home inspection evaluates the physical condition of the property for the buyer. Both are separate and serve different purposes.