TL;DR:

- Leverage allows control of high-value properties with limited cash in Southern California.

- Higher LTV ratios increase potential returns but also amplify risk and vulnerability to market declines.

- Successful investors use leverage selectively, focusing on property fundamentals and strong market conditions.

Most people assume that buying real estate in Southern California requires either deep pockets or years of saving. That assumption stops a lot of would-be buyers and investors from ever getting started. The truth is that leverage, which means using borrowed money to control a property, lets you put relatively little cash down and still benefit from the full appreciation of the asset. A buyer who puts $100,000 down on a $1,000,000 home in Los Angeles gains from every dollar that home increases in value, not just the dollars they contributed. This article breaks down exactly how leverage works, when it helps you, when it hurts you, and how to use it strategically in one of the most competitive real estate markets in the country.

Table of Contents

- What is leverage in real estate?

- How leverage amplifies returns—and risk

- When does leverage work for you? Positive vs. negative leverage explained

- Assessing risk: What most investors overlook

- Smart leverage strategies for Southern California buyers and investors

- The real value of leverage: Our perspective for 2026

- Take your next step in Southern California real estate

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Leverage magnifies outcomes | Using borrowed money can increase both gains and losses in real estate. |

| Positive leverage is key | Returns rise when the property's rate of return is higher than the loan's interest rate. |

| Risk discipline is required | Stress-test deals and avoid overextending, especially in fast-moving areas like Southern California. |

| Options vary by property type | Loan limits and down payment requirements differ for homes, investments, and multifamily deals. |

What is leverage in real estate?

Leverage in real estate simply means using a loan to purchase a property instead of paying the full price in cash. You put down a portion of the purchase price, borrow the rest from a lender, and then control the entire asset. The ratio of the loan to the total property value is called the loan-to-value ratio, or LTV. A high LTV means you borrowed most of the purchase price. A low LTV means you put more cash in and borrowed less.

Here's why this matters so much in Southern California. Median home prices in Los Angeles and Orange County regularly exceed $800,000 and can stretch well past $1,500,000 in desirable neighborhoods. Very few buyers can pay cash outright. Leverage is not just a tool for savvy investors. It is the practical mechanism that makes homeownership possible for most families in this market.

For primary residences, LTV limits reach 95% with FHA and conventional loan programs, meaning a buyer needs as little as 5% down. Investment properties are typically capped at 75% to 85% LTV, and multifamily agency loans fall in the 75% to 80% range. These limits reflect lender risk tolerance and shape your strategy depending on whether you're buying a home to live in or building a rental portfolio.

The power of leverage is in how it stretches your capital. Consider this example from a realistic Southern California scenario. You have $50,000 in savings. Without leverage, you might purchase a small property outright in a tertiary market. With leverage in Southern California, that same $50,000 could serve as a down payment on a property worth $500,000 to $700,000, giving you exposure to a far more valuable asset and all the appreciation that comes with it.

Here are the most common ways buyers and investors use leverage in this market:

- Primary homeownership: Use FHA or conventional financing to buy a home with 3.5% to 10% down, gaining full exposure to appreciation and building equity over time.

- Single-family rentals: Use a 20% to 25% down investment loan to acquire a rental property, then use rental income to cover the mortgage.

- House hacking: Buy a duplex or triplex, live in one unit, and rent the others to offset or eliminate your mortgage payment.

- Portfolio expansion: Refinance an appreciated property to pull out equity and use it as a down payment on another.

- Real estate crowdfunding: Participate in leveraged real estate deals with lower capital requirements by pooling resources with other investors.

"The best investment on Earth is earth." That sentiment rings especially true in Southern California, where land scarcity and population density have kept values climbing for decades, making leverage an even more powerful tool when used thoughtfully.

The fundamental rule of leverage is simple: you win bigger when the property appreciates, but you also lose bigger if values fall or carrying costs rise. Understanding that duality is the foundation of every smart leverage decision.

How leverage amplifies returns—and risk

Let's get into the math, because this is where leverage gets genuinely compelling. Suppose you buy a $1,000,000 home in Pasadena and it appreciates by 5% over one year. The property is now worth $1,050,000. Your gain is $50,000.

Now consider two scenarios. In the first, you paid all cash. Your return is $50,000 on a $1,000,000 investment, which is a 5% return. In the second scenario, you put 10% down ($100,000) and borrowed the rest. You still gained $50,000 in property value, but that gain is on your $100,000 equity investment. That's a 50% return. Same property. Same appreciation. Dramatically different return on invested capital.

This is the core insight in leveraged investing: a 5% property gain at 90% LTV can yield approximately 50% equity return, but risk scales proportionally, and stress-testing for rate rises and vacancy is non-negotiable.

Here is a straightforward comparison of outcomes under different LTV and interest rate combinations:

| LTV | Down payment | Property value gain (5%) | Equity return | Monthly rate risk (if rates rise 1%) |

|---|---|---|---|---|

| 50% | $500,000 | $50,000 | 10% | Minimal |

| 75% | $250,000 | $50,000 | 20% | Moderate |

| 90% | $100,000 | $50,000 | 50% | Significant |

| 95% | $50,000 | $50,000 | 100% | Very high |

The higher your LTV, the greater your potential return, but also the greater your exposure to problems. If your property drops in value, a high LTV means you lose a larger percentage of your actual invested cash.

Here are the steps to calculate your potential leveraged gain or loss on any Southern California property:

- Identify your down payment and calculate your LTV percentage.

- Project the property's appreciation using historical averages for that specific market, neighborhood, or zip code.

- Subtract your financing costs including interest, insurance, and taxes for the holding period.

- Calculate net equity gain by dividing profit by your actual cash invested.

- Run a downside scenario assuming 5% to 10% value decline and rising interest rates to see how your equity holds up.

Risk rises sharply with leverage for three primary reasons. First, you have fixed payment obligations regardless of what the market does. Second, vacancy in a rental property can leave you covering the full mortgage from your own pocket. Third, equity swings become magnified. A 10% drop on a $1,000,000 property wipes out an entire $100,000 down payment at 90% LTV.

Pro Tip: Before committing to any leveraged deal, always stress-test it with two scenarios: a 15% to 20% price correction and a mortgage rate increase of 1.5 to 2 percentage points. If you can still cover your obligations in those scenarios, your leverage level is defensible. Explore prime investment areas in SoCal where fundamentals can help cushion that downside.

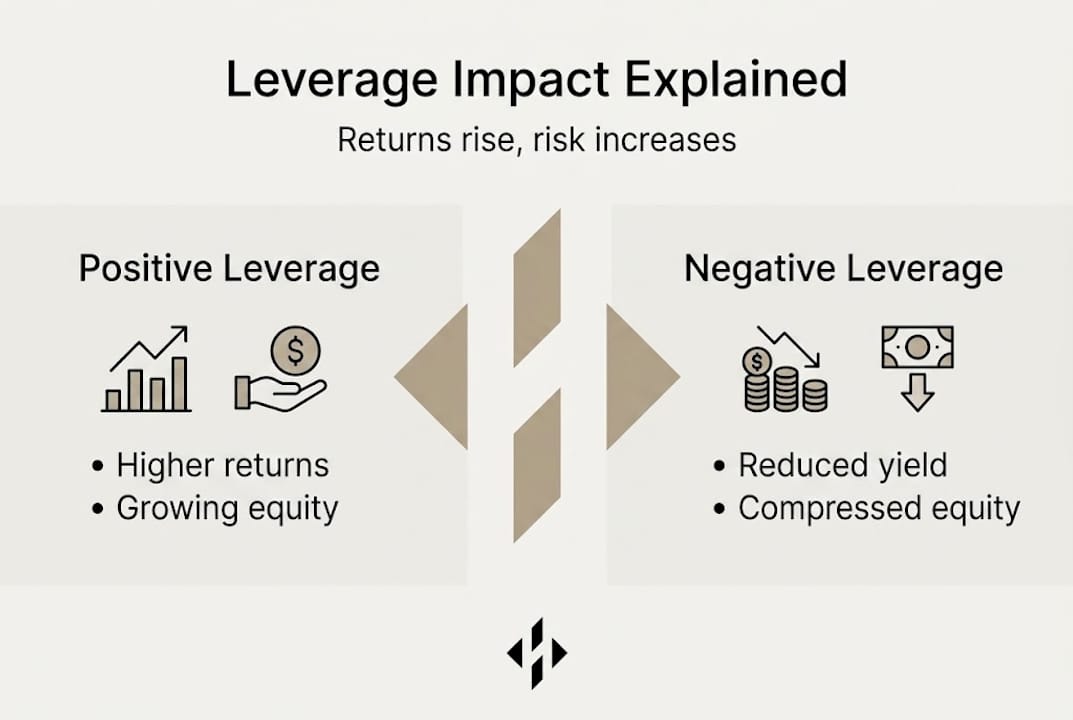

When does leverage work for you? Positive vs. negative leverage explained

Understanding positive versus negative leverage is what separates sophisticated real estate investors from those who stumble into bad deals. These terms have precise, mathematical definitions, and knowing them will change how you evaluate every property.

Positive leverage happens when the return you earn on the property exceeds the cost of your debt. If a rental property in Long Beach generates a 7% cap rate (net operating income divided by purchase price) and your loan costs you 5.5% annually, you're earning more from the asset than you're paying to finance it. That spread flows to your equity and increases your overall return.

Positive leverage at 80% LTV can transform a 5% unlevered cash-on-cash return into 20% or more, which is the mathematical argument for using financing even when you could pay cash.

Here's a practical data comparison for Southern California scenarios:

| Scenario | Cap rate | Debt cost | LTV | Cash-on-cash return | Leverage effect |

|---|---|---|---|---|---|

| All cash | 5.5% | None | 0% | 5.5% | None |

| Conservative | 5.5% | 5.0% | 70% | 8.5% | Positive |

| Aggressive | 5.5% | 7.0% | 80% | 3.2% | Negative |

| Moderate | 6.5% | 5.5% | 75% | 10.8% | Positive |

Negative leverage occurs when your debt cost exceeds the property return, which reduces your equity yield and compresses cash flow. Negative leverage reduces equity yield and cash flow, but can still be viable if you're buying at a discount with strong appreciation or value-add potential ahead.

This is a subtle but important point. A property with a 4.5% cap rate and a 7% mortgage rate is technically in negative leverage territory. But if you're buying in a supply-constrained neighborhood in Culver City or Santa Monica where appreciation historically runs at 6% to 8% annually, the total return can still justify the deal. It's not a black-and-white rule.

Here is how to spot positive versus negative leverage before you buy:

- Compare cap rate to your all-in debt cost. If cap rate is higher, you're in positive territory.

- Look at the debt service coverage ratio (DSCR). A DSCR above 1.25 means the property covers its loan comfortably.

- Factor in appreciation forecasts. In high-growth SoCal neighborhoods, total return includes appreciation, not just income yield.

- Review local rent growth data. Rising rents improve future returns and can flip a currently negative deal into a positive one over time.

- Model exit scenarios. Run at least three exit timelines (3, 5, and 10 years) to see when leverage becomes favorable given your purchase price.

Understanding the benefits of buying a home in LA goes hand-in-hand with knowing how leverage interacts with specific submarkets, where appreciation rates, rental demand, and supply constraints all shape whether your financing structure helps or hurts you.

Assessing risk: What most investors overlook

Armed with the how and why of leverage, let's address the crucial question: What can go wrong, and how do you protect yourself?

The most common mistake leveraged investors make in Southern California is modeling best-case scenarios and forgetting that real estate markets move in cycles. The current environment, where debt costs rose sharply from 2022 through 2024 before stabilizing, illustrated exactly how quickly leverage can shift from friend to burden.

The key risks to monitor in any leveraged deal include:

- Vacancy: A vacant rental unit in a high-LTV deal can eat through reserves in weeks. Even in strong markets like Orange County, unexpected vacancies happen.

- Rising interest rates: If you hold an adjustable-rate mortgage, a rate spike directly increases your monthly payment and narrows your margin.

- Market value declines: Southern California has experienced significant corrections, including the early 1990s downturn when some markets fell 20% to 30%, and again in 2008 to 2010.

- Equity swings: At 90% LTV, a 10% market correction leaves you with zero equity. At 80% LTV, you still have a 10% equity cushion.

- Liquidity crunch: Highly leveraged properties require ongoing cash reserves. If you're overextended, one bad month can cascade into a serious problem.

Leverage functions as a risk redistributor, not a value creator. It amplifies equity volatility rather than creating additional value from the property itself, and this is a distinction worth internalizing deeply.

Recent market data reinforces this point. As debt costs have risen and compressed spreads, the value of leverage in real estate has declined, shifting focus back to core property performance rather than capital structure optimization.

Pro Tip: Build a risk checklist for every deal before signing. Include breakeven occupancy rate, debt service coverage at current and stressed rates, maximum tolerable vacancy period, equity buffer at various market decline scenarios, and your liquidity reserve runway in months.

Protecting yourself starts with smart sourcing. Off-market deals and leverage go well together because off-market properties often come with more negotiating room, which gives you a better entry price and a natural cushion against downside. A skilled agent who understands risk management in Southern California can help you identify these opportunities. And before any deal closes, a thorough property valuation ensures your leverage is based on accurate numbers rather than inflated comps.

Smart leverage strategies for Southern California buyers and investors

Understanding risks and rewards is vital, but here are proven strategies to put the power of leverage to work for your goals in today's market.

For homebuyers, the primary leverage tools are FHA and conventional loans. FHA loans allow up to 95% LTV for primary residences, while conventional programs typically go to 95% as well with private mortgage insurance. Investment properties are generally capped at 75% to 85% LTV depending on the lender and property type. Multifamily agency loans, which cover two to four unit properties through Fannie Mae and Freddie Mac, commonly reach 75% to 80% LTV.

For investors, the smartest leverage strategy balances LTV with property fundamentals. Chasing the maximum possible loan amount in a market like 2026 Southern California, where debt costs remain elevated relative to historical norms, is a recipe for negative leverage. A 70% to 75% LTV on a well-located rental property with strong rent growth potential is often a better position than 85% LTV on a marginal asset.

Here are the steps to stress-test your leverage plan before committing:

- Get a pre-approval that confirms your actual borrowing capacity and interest rate range.

- Run a baseline cash flow model using current rent market data for the specific zip code.

- Apply a 10% rent reduction to your model to simulate a soft rental market.

- Increase your assumed interest rate by 1.5% to see how sensitive your deal is to rate movements.

- Model a 15% property value decline and calculate what your equity position looks like at that point.

- Calculate your breakeven occupancy rate to know what minimum tenancy keeps you cash-flow neutral.

- Confirm your reserve fund covers at least six months of full mortgage payments and maintenance costs.

Leverage dos and don'ts for Southern California buyers and investors:

- Do match your LTV to the quality of the asset. Better assets support higher leverage.

- Do build cash reserves before increasing your leverage. A 6-month reserve is a minimum, not a luxury.

- Do prioritize neighborhoods with low vacancy rates and strong employment bases, such as areas near tech, healthcare, and entertainment hubs.

- Don't use maximum leverage just because a lender approves it. Approval is not the same as wisdom.

- Don't ignore the impact of property taxes, insurance, and HOA fees when calculating real returns.

- Don't let FOMO (fear of missing out) drive you into an overleveraged position in a bidding war.

Exploring essential SoCal investment tips alongside your leverage plan will sharpen your market read. And if you're still evaluating whether this market fits your goals, reviewing the core reasons to invest in SoCal will give you broader context for the opportunity in front of you.

The real value of leverage: Our perspective for 2026

Here's what years of working in Southern California real estate have genuinely taught us about leverage: most buyers and investors treat it like a volume knob. They think the answer to building wealth faster is simply to turn it up. That's the mistake.

The investors who actually compound wealth in this market over time aren't the ones who maximize leverage on every deal. They're the ones who use leverage selectively, only when the property fundamentals justify it and when they can absorb the downside without a crisis.

The current market environment reinforces this lesson sharply. As debt costs climbed from historically low levels to present rates, every leveraged deal became more sensitive to property performance. The buffer that cheap financing once provided is narrower now. That means the property itself, its location, its tenant quality, its rent growth potential, has to carry more of the weight. Capital structure alone no longer compensates for a mediocre asset.

What experienced investors in Southern California are doing differently in 2026 is focusing on quality over quantity of leverage. They're buying fewer deals at more conservative LTV levels, in neighborhoods with durable demand drivers, and holding longer. They're also using leverage to free up capital for diversification, not to overextend on a single bet. Risk discipline is not the enemy of returns. It's what allows returns to actually accumulate over a full market cycle.

We explore investment lessons for 2026 in depth elsewhere, but the core message is this: leverage is a tool. Like any tool, it magnifies both skill and error. Use it with intention, not instinct.

Take your next step in Southern California real estate

You now understand how leverage works, when it adds value, and where it can hurt you. The next step is applying that knowledge to a real property in a real Southern California market, with the right data and the right guidance behind your decision.

At increaltors.com, we specialize in helping Southern California buyers and investors navigate exactly these decisions. From detailed property listings across Los Angeles and Orange County to personalized market evaluations, our platform gives you the tools to identify the right leverage opportunities and avoid the common pitfalls. Whether you're buying your first home with an FHA loan or building a rental portfolio across multiple neighborhoods, our team, led by agent Irvin Nierras, brings local market expertise directly to your strategy. Explore our current listings, request a home valuation, or connect directly with us to talk through your leverage plan and find properties that align with your goals in today's market.

Frequently asked questions

What is a safe level of leverage for first-time homebuyers?

Most experts suggest staying below 90% to 95% LTV for primary residences, and between 75% to 85% for investment properties, in line with FHA and conventional loan program limits. Keeping reserves of at least six months of mortgage payments adds an important additional safety layer.

How does rising interest rates affect leveraged real estate investments?

Higher interest rates narrow the spread between property returns and debt costs, often reducing or eliminating the advantage of leverage. As debt costs compress spreads, investors must rely more heavily on the property's own performance metrics to justify their capital structure.

Can negative leverage ever make sense for investors?

Yes, particularly in supply-constrained Southern California markets where strong appreciation is a realistic expectation. Negative leverage can still yield solid total returns if you're buying at a discount with a clear value-add strategy or in a neighborhood with consistent historical appreciation above debt cost levels.

Do Southern California markets present unique risks when using leverage?

Absolutely. SoCal markets move in pronounced cycles, with sharp appreciation phases followed by meaningful corrections. The combination of high entry prices, elevated property taxes, and competitive lending conditions means any leveraged deal requires particularly rigorous stress-testing and conservative reserve planning to weather market volatility.