TL;DR:

- Home loan pre-approval in West Covina involves verified documentation, a hard credit check, and stable finances, boosting your offer’s credibility.

- You must prepare all necessary documents beforehand and avoid financial changes after receiving your preapproval to ensure smooth approval through closing.

Home loan pre-approval in West Covina is the process where a lender verifies your income, assets, and credit history, then conditionally approves a specific loan amount before you begin shopping for a home. This is the industry term for what many buyers call "getting pre-approved for a mortgage," and it carries far more weight with sellers than a basic prequalification. Lenders like SoFi and Freedom Mortgage distinguish sharply between the two: preapproval involves verified documentation and a hard credit inquiry, while prequalification relies on self-reported numbers and a soft check. For first-time buyers competing in West Covina's San Gabriel Valley market, that distinction can determine whether your offer gets accepted or ignored.

What documents do you need for home loan pre-approval in West Covina?

Preparation is the single factor that separates buyers who get their preapproval letter in three days from those who wait three weeks. Lenders need a complete financial picture before they can issue a conditional approval, and missing even one document can push your timeline back significantly. According to Cole Brantley Mortgage, missing papers delay approvals by 7 to 14 days. That is a costly gap when you are watching a listing you want.

Income verification documents

Your lender will ask for recent pay stubs covering the last 30 days, W-2 forms from the past two years, and federal tax returns for the same period. Self-employed buyers need to provide 1099s and a profit-and-loss statement prepared by a CPA. If you receive bonus income, commission, or overtime, lenders typically average those figures over 24 months rather than using the most recent year alone.

Bank and asset statements

Two months of complete bank statements are standard, and "complete" means every page, including the blank ones. Underwriters flag incomplete submissions immediately. Investment accounts, retirement funds like a 401(k) or IRA, and any other liquid assets should also be included. Clear source of funds verification is a critical underwriting concern, so any large deposit outside your regular paycheck will require a written explanation and supporting documentation.

Additional documents for first-time buyers

Beyond income and assets, you will need a government-issued photo ID and your Social Security number for the credit pull. If a family member is gifting you part of the down payment, a signed gift letter stating the funds are not a loan is required. Some lenders also request a rental history or landlord contact information if you have never held a mortgage before.

Here is a quick checklist to gather before you apply:

- Recent pay stubs (last 30 days)

- W-2 forms for the past two years

- Federal tax returns for the past two years

- Two months of complete bank statements

- Investment and retirement account statements

- Government-issued photo ID

- Gift letter (if applicable)

- Explanation letters for any large or unusual deposits

Pro Tip: Scan every document as a multi-page PDF before you apply. Lenders using digital portals like Encompass or SimpleNexus will process your file faster when everything arrives in one organized upload rather than scattered email attachments.

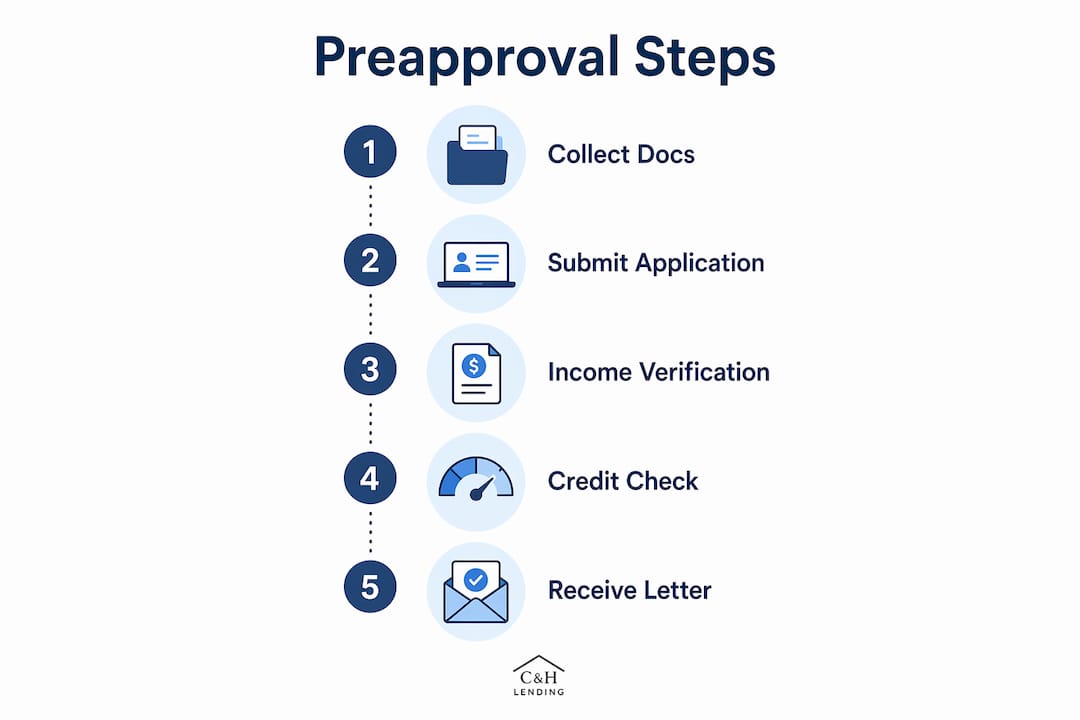

How to apply and get your mortgage preapproval step by step

The West Covina mortgage pre-approval process follows a predictable sequence once you have your documents ready. Understanding each stage removes the anxiety of waiting and helps you respond to lender requests without delay. Freedom Mortgage outlines the standard preapproval workflow as application, document submission, credit and debt-to-income review, and then issuance of a conditional approval letter.

Here is how the process unfolds in practice:

- Choose your lender and loan type. West Covina home loan options include conventional loans, FHA loans (which allow down payments as low as 3.5%), VA loans for eligible veterans, and USDA loans for qualifying rural-adjacent properties. Compare at least three lenders, including local credit unions, regional banks, and national lenders, before committing.

- Submit your application. Most lenders offer online applications through portals like Blend or Encompass, but you can also apply by phone or in person. The application captures your employment history, income, monthly debts, and the property type you intend to buy.

- Authorize the credit pull. The lender will run a hard inquiry on your credit report through Equifax, TransUnion, or Experian. Multiple mortgage inquiries within a 14 to 45-day window are typically treated as a single inquiry under FICO scoring models, so shopping multiple lenders in that window does not significantly hurt your score.

- Lender reviews your debt-to-income ratio. Most conventional lenders cap the debt-to-income ratio at 43 to 45 percent. FHA loans allow up to 57 percent in some cases. Your lender's automated underwriting system, either Fannie Mae's Desktop Underwriter or Freddie Mac's Loan Product Advisor, generates a conditional approval based on these figures.

- Receive your preapproval letter. The letter states the approved loan amount, loan type, interest rate assumption, and any conditions you must satisfy before final approval. Read every condition carefully.

The table below shows how the most common West Covina home loan options compare at the preapproval stage:

| Loan Type | Minimum Credit Score | Minimum Down Payment | Key Requirement |

|---|---|---|---|

| Conventional | 620 | 3% to 5% | Private mortgage insurance below 20% down |

| FHA | 580 | 3.5% | Mortgage insurance premium required |

| VA | No set minimum | 0% | Military service eligibility required |

| USDA | 640 | 0% | Property must be in eligible rural area |

Pro Tip: Ask your lender whether your preapproval was run through an automated underwriting system and whether it generated a specific approval finding. A letter backed by a Desktop Underwriter approval is significantly stronger than a generic letter based on a loan officer's manual review.

Organizing and submitting complete financial documents upfront reduces lender follow-up requests and accelerates the timeline from application to letter. Most buyers who prepare thoroughly receive their letter within three to five business days.

How to protect your preapproval after you receive it

Receiving your preapproval letter is not the finish line. It is a conditional commitment, and lenders re-verify your financial profile before closing. The period between preapproval and closing is where many first-time buyers unknowingly damage their own approval. Dwell Mortgage describes this as a financial freeze period, meaning you avoid any major financial changes until the keys are in your hand.

The most common mistakes that derail approvals after the letter is issued include:

- Opening new credit accounts. A new credit card or auto loan raises your debt-to-income ratio and lowers your average account age. Both hurt your mortgage qualification.

- Making large purchases on existing credit. Buying furniture, appliances, or a car on credit before closing changes your monthly obligations and can push your debt-to-income ratio above the lender's threshold.

- Changing jobs or income structure. Switching from salaried to self-employed, or even changing employers within the same industry, triggers re-verification. Lenders want to see stability, not transition.

- Missing any bill payments. A single 30-day late payment on a credit card or utility account can drop your credit score enough to change your loan terms or void approval entirely.

- Making unexplained large deposits. Depositing a large sum of cash or receiving a wire transfer without documentation raises underwriting flags about the source of funds.

"After preapproval, treat your finances like you are under audit. Every dollar moved, every account opened, and every bill paid is visible to your lender before closing." — Onshore Mortgage

Opening new credit or large purchases after preapproval can derail underwriting before closing. This is not a theoretical risk. It happens regularly to buyers who assume the hard work is done once the letter arrives.

Most preapproval letters expire within 60 to 90 days. If your home search extends beyond that window, your lender will require updated pay stubs, bank statements, and a new credit pull to renew the letter. Plan your home search timeline accordingly, especially in a market like West Covina where well-priced inventory can move in days.

Pro Tip: Tell your lender immediately if anything changes in your financial situation after preapproval. Proactive disclosure is far better than a lender discovering a change during final underwriting, when options to correct course are limited.

How a strong preapproval letter affects your offer in West Covina

Not all preapproval letters carry the same weight with sellers and listing agents. A letter that reflects thorough verification and automated underwriting approval signals to a seller that your financing is solid. A generic letter that simply states "this buyer may qualify for up to X amount" based on a brief phone conversation tells a seller almost nothing. In West Covina's competitive real estate market, that difference can determine whether your offer gets accepted over a competing bid.

The table below compares a lightly verified preapproval letter against a thoroughly verified one:

| Factor | Light Verification | Thorough Verification |

|---|---|---|

| Income check | Self-reported | Pay stubs and W-2s reviewed |

| Credit pull | Soft inquiry only | Hard inquiry completed |

| Underwriting | Manual estimate | Automated system approval |

| Seller confidence | Low to moderate | High |

| Offer competitiveness | Weak | Strong |

Lenders' automated underwriting systems generate conditional approval letters that specify assumptions and pending conditions, making them more credible than generic preapproval letters. Sellers and their agents know the difference, and in multiple-offer situations, a listing agent will advise their client to favor the buyer with the stronger financing documentation.

When you present your preapproval letter with an offer, include the letter amount calibrated to the offer price rather than your maximum approved amount. Showing a seller your full borrowing capacity gives away negotiating leverage. Work with your real estate agent to present the letter in a way that confirms your qualification without revealing your ceiling. For more on how to present your financing effectively, the real estate offer process in Southern California provides practical guidance from professionals who negotiate these situations regularly.

Understanding the difference between prequalification and preapproval helps buyers shop smarter with realistic expectations. A buyer who walks into a West Covina open house with a verified preapproval letter is treated differently by agents, sellers, and even competing buyers. That credibility is built before you ever set foot in a property.

Key takeaways

Home loan pre-approval in West Covina requires verified documentation, a hard credit pull, and stable finances from application through closing to give your offer real competitive strength.

| Point | Details |

|---|---|

| Preapproval beats prequalification | Verified income, assets, and a hard credit pull make your offer credible to West Covina sellers. |

| Document preparation is critical | Missing one document can delay your preapproval by 7 to 14 days, so gather everything before applying. |

| Protect your finances post-approval | Avoid new credit, large purchases, and job changes between preapproval and closing to keep your conditional approval intact. |

| Letters expire in 60 to 90 days | Plan your home search timeline so you are not forced to renew documentation mid-negotiation. |

| Automated underwriting strengthens offers | A letter backed by Desktop Underwriter or Loan Product Advisor approval carries more weight than a manual estimate. |

What I have learned helping West Covina buyers get preapproved

The mistake I see most often is buyers treating preapproval as a formality they handle the week they want to make an offer. By then, they are already behind. The buyers who move fastest and win the homes they want start the preapproval process 60 to 90 days before they plan to buy. That window gives them time to correct credit issues, source a down payment properly, and choose a lender who actually knows how to close on time.

West Covina attracts a lot of first-time buyers because it sits at a price point that feels accessible compared to Arcadia or San Marino, but the competition is real. I have watched buyers lose homes they loved because their preapproval letter was not credible enough for the listing agent to recommend accepting their offer over a slightly lower bid with stronger financing documentation.

My honest advice on choosing a lender: do not default to your personal bank out of convenience. Compare a local credit union like Arrowhead Credit Union, a regional lender, and a national lender. Ask each one specifically whether they use Desktop Underwriter or Loan Product Advisor, and ask how long their average preapproval takes. A lender who takes ten business days to issue a letter in a market where homes go pending in five days is not the right partner for you.

Treat your preapproval as a conditional commitment, not a guarantee. Your financial behavior between that letter and closing is just as important as the work you did to earn it. If you are preparing to buy in West Covina, start with the first-time buyer tips for Southern California that Increaltors has put together. The sequence matters, and getting it right from the start saves you time, money, and real stress.

— Irvin Nierras

Start your West Covina home search with Increaltors

Once your preapproval letter is in hand, the next step is finding the right property in West Covina before someone else does. Increaltors, led by agent Irvin Nierras of HomeSmart Evergreen Realty, works directly with first-time buyers to match their preapproved budget with available inventory in the San Gabriel Valley. Whether you are looking for a single-family home or want to understand what your budget realistically gets you in today's market, Increaltors provides personalized guidance from the first conversation through closing. Browse current West Covina home listings or explore single-family homes for sale to see what is available right now. Contact Irvin Nierras directly to schedule a consultation and put your preapproval to work.

FAQ

What is the difference between prequalification and preapproval?

Prequalification uses self-reported financial data and a soft credit check to estimate what you might borrow. Preapproval requires verified income, asset documentation, and a hard credit inquiry, making it a far more credible signal to sellers.

How long does home loan pre-approval take in West Covina?

Most buyers who submit complete documentation receive a preapproval letter within three to five business days. Missing documents can extend that timeline by 7 to 14 days, so preparation before applying is critical.

How long is a mortgage preapproval letter valid?

Most preapproval letters are valid for 60 to 90 days. If your home search extends beyond that window, your lender will require updated documents and a new credit pull to renew your approval.

Will getting preapproved hurt my credit score?

A single mortgage preapproval triggers a hard inquiry, which may lower your score by a few points temporarily. Multiple mortgage inquiries within a 14 to 45-day window are typically counted as one inquiry under FICO scoring models, so shopping multiple lenders in that period has minimal impact.

What can void my preapproval before closing?

Opening new credit accounts, making large purchases, changing jobs, missing bill payments, or making unexplained large deposits can all trigger re-verification or void your conditional approval before closing. Maintaining a financial freeze from preapproval through closing protects your loan status.