TL;DR:

- Homebuyers in Southern California often overestimate the home's true value, which is determined by licensed appraisers.

- Appraisals are crucial because they protect lenders and influence deals, especially when market prices fluctuate dramatically.

Many homebuyers in Southern California assume the agreed purchase price is the home's true value. It isn't. Your lender, your agent, and ultimately the deal itself all hinge on a number determined by a licensed appraiser, and that number can be thousands of dollars away from what you wrote on your offer. In a market where Los Angeles and Orange County median prices routinely exceed $800,000, a gap between price and appraised value is not a technicality. It can kill a deal, reopen negotiations, or leave a buyer scrambling to cover cash at closing. This guide explains exactly what a home appraisal is, how the process works, what factors drive value in SoCal, and how you can use that knowledge to your advantage.

Table of Contents

- What is a home appraisal and why does it matter?

- The home appraisal process: step by step

- Key factors appraisers evaluate in Southern California

- Challenges and edge cases in home appraisals

- What's driving home values in SoCal in 2026?

- The real story: why accurate appraisals make (or break) SoCal deals

- Ready to make your next move? Get local expertise

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Appraisal defines value | The home appraisal sets your property’s value for lenders, not just your asking price. |

| Southern California is unique | Diverse neighborhoods and rapid market shifts make local expertise essential for appraisals. |

| Key factors matter most | Location, upgrades, condition, and comparable sales are what appraisers weigh most carefully. |

| Be ready for surprises | Appraisals can reveal challenges, especially with unique properties or in hot markets. |

| Market trends influence value | 2026’s rising prices and low affordability make understanding your appraisal even more important. |

What is a home appraisal and why does it matter?

A home appraisal is a formal, unbiased estimate of a property's market value conducted by a licensed or certified appraiser. It is not the same as a home inspection, a Zillow estimate, or your neighbor's opinion about what your street is worth. The appraisal produces a written report, backed by data and regulatory standards, that tells a lender what a property is actually worth as collateral.

The primary purpose is to protect lenders by ensuring the home's value supports the mortgage amount, and it is required in most purchases, refinances, and other financing arrangements. That single sentence explains why appraisals matter so much. If a lender is handing you $900,000 to buy a home, they need independent proof that the home is actually worth $900,000. If it comes in at $850,000, you have a problem.

Everyone involved in the transaction has a stake in the appraisal:

- Buyers need the appraised value to support their financing, or they risk paying more than the home is worth

- Sellers want the appraisal to confirm their asking price so the deal does not fall apart or require a price cut

- Lenders use it to set loan limits and manage risk on their investment

- Real estate agents use it to set realistic expectations and frame negotiations

Understanding the role of home appraisers in a Southern California transaction is especially important because the market moves fast and prices vary dramatically by block, not just by city. A property in Arcadia and one two miles away in Temple City can carry very different values even if the homes look nearly identical. The appraiser is the person responsible for capturing that distinction accurately.

"The appraisal is not there to validate the seller's wish list or the buyer's excitement. It is there to establish what the market would actually pay under normal conditions."

The legal and regulatory framework behind appraisals also matters. All residential appraisals for federally backed loans must comply with the Uniform Standards of Professional Appraisal Practice, commonly called USPAP. These standards govern methodology, ethics, reporting, and disclosure, creating a consistent baseline that protects buyers and sellers alike.

The home appraisal process: step by step

Once you understand why an appraisal happens, the next logical question is how it happens. The process is more structured than most buyers realize, and knowing each stage helps you avoid delays and surprises.

- Order and scheduling. After a purchase contract is signed or a refinance application is submitted, the lender orders the appraisal through an Appraisal Management Company (AMC) or directly from an appraiser. The appraiser then contacts the homeowner or listing agent to schedule the on-site visit.

- On-site inspection. The appraiser visits the property and physically inspects the interior and exterior. They measure rooms, photograph the home, and note condition, finishes, and any obvious deficiencies. A typical inspection takes one to three hours.

- Comparable sales research. After the site visit, the appraiser pulls recent sales of similar properties, called comparables or "comps," from the local area. They look for homes that sold within the past three to six months, in the same neighborhood or a similar one, with comparable size and features.

- Adjustments and analysis. No two homes are identical. The appraiser makes dollar adjustments to each comp to account for differences in square footage, bedroom count, lot size, condition, and amenities. This is where judgment and expertise matter most.

- Report preparation. The appraiser compiles everything into a formal report, most commonly a Uniform Residential Appraisal Report (URAR), and submits it to the lender.

- Lender review and delivery. The lender reviews the report and forwards a copy to the buyer. Federal law requires lenders to share the full appraisal report with the borrower.

Pro Tip: If you are a seller preparing for an appraisal, clean the home thoroughly, fix minor deficiencies like broken fixtures or damaged trim, and compile a list of all upgrades with costs and dates. Giving the appraiser clear documentation helps them make accurate, favorable adjustments.

The SoCal appraisal guide for Los Angeles and Orange County buyers dives deeper into regional timing, but generally you can expect the report to be completed within 5 to 10 business days after the on-site inspection.

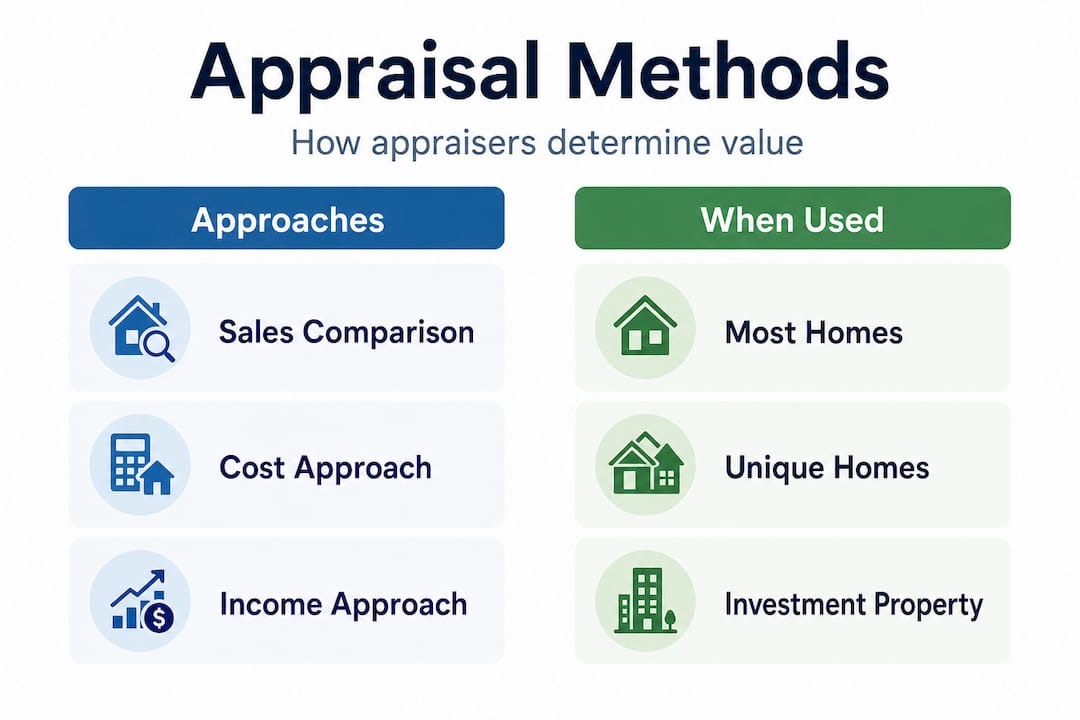

When it comes to methodology, appraisers rely on three main approaches. Understanding the differences helps you see how your specific property type will be evaluated.

| Appraisal method | When it is used | How it works |

|---|---|---|

| Sales comparison approach | Most residential homes | Adjusts recent comp sales to match subject property |

| Cost approach | New construction, unique properties | Estimates land value plus cost to rebuild minus depreciation |

| Income approach | Rental or investment properties | Capitalizes the property's net income into a value |

Key methodologies such as the sales comparison approach, cost approach, and income approach are supported by statistical tools like regression analysis and paired sales analysis to ensure adjustments are defensible. In SoCal, the sales comparison approach is the dominant method for single-family homes, but the income approach becomes relevant quickly given how many homeowners rent out ADUs or investment units.

Key factors appraisers evaluate in Southern California

The physical inspection and comp research are only part of the picture. Appraisers weigh a specific set of criteria to arrive at their final number, and in Southern California, some of those criteria carry unusual weight.

Appraisers evaluate a wide range of factors including location, size, age, condition, upgrades, major systems like the roof and HVAC, neighborhood characteristics, and comparable sales data. All room measurements are taken according to ANSI standards to ensure consistency across reports.

Here is how those factors play out in the Southern California context:

- Location and neighborhood. In SoCal, a few blocks can separate premium coastal pricing from inland suburban values. An appraiser in Huntington Beach will consider beach proximity as a value driver in ways that simply do not apply in the San Fernando Valley.

- Square footage and layout. Larger homes generally appraise higher, but layout matters too. Open-concept homes with modern flow often outperform dated layouts of the same size.

- Age and condition. Homes built in different eras carry different structural considerations. A 1920s Craftsman in Pasadena is evaluated very differently than a 2005 stucco build in Chino Hills.

- Upgrades and renovations. Kitchen and bath upgrades typically carry the strongest value adjustments. However, the appraiser checks whether the renovation quality matches the neighborhood standard. A luxury remodel in a starter-home area may not return full investment.

- Major systems. Roof age, HVAC condition, electrical panel type, and plumbing materials are all noted. Older systems or flagged safety issues can lower the appraisal.

Pro Tip: If your home has an Accessory Dwelling Unit (ADU), make sure it was permitted. Unpermitted ADUs may not be counted in square footage or income analysis, which can significantly reduce appraised value compared to what you expect.

In Southern California, diverse neighborhoods, complex zoning, and coastal influences require exceptionally careful comp selection, and all appraisals must follow USPAP standards to maintain credibility and legal standing.

| SoCal-specific feature | How it affects value |

|---|---|

| Permitted ADU | Adds income potential; may increase value by $50K or more |

| Ocean or mountain view | Can add 5% to 20% depending on quality and comparables |

| Coastal zone location | May trigger special valuation adjustments and zoning review |

| Historic district designation | Can restrict renovations; affects comp pool |

If you have questions about how local characteristics affect your property's value, the right questions for SoCal agents can surface insights that generic online tools never will. For buyers navigating this for the first time, reading through first-time buyer tips specific to this region can sharpen your preparation before the appraisal visit.

Challenges and edge cases in home appraisals

Even experienced buyers and sellers are sometimes blindsided when an appraisal gets complicated. Here are the scenarios that most commonly cause problems in the Southern California market.

Unique or custom homes. Appraisers depend on comparable sales. When a home is truly one of a kind, whether it is a custom architectural build, a historic property, or an unusually large estate, finding accurate comps becomes difficult. The appraiser may need to stretch their search area or time window, which introduces uncertainty into the final value.

Thin markets. In some neighborhoods, so few homes sell in a given period that the appraiser simply does not have enough data. This happens in ultra-luxury segments, rural pockets on the SoCal fringe, and hyper-specific condo buildings where units rarely turn over.

Rapidly appreciating or declining markets. Real estate appraisals are rooted in recent sales data, which means they inherently lag the market. During a fast run-up in prices, like SoCal saw during the pandemic years, appraisals sometimes came in below the contract price simply because the comps had not caught up. In a declining market, the same lag can work the other way.

Edge cases including unique homes, thin markets, rapid appreciation, condition issues, and non-disclosure scenarios challenge automated valuation models, but a licensed appraiser conducting a full inspection and analysis is far better equipped to handle these situations accurately.

Condition issues discovered on-site. If the appraiser observes significant damage, moisture intrusion, or safety hazards during the inspection, they can flag the property as subject to repairs. In those cases, the final value may be conditioned on specific repairs being completed before the loan closes. This creates a timeline problem for buyers and sellers who are already in escrow.

"A low appraisal does not automatically end a deal. It opens a conversation. The question is whether all parties are willing to have it honestly."

California is a non-disclosure state for many property details, meaning sellers are not always required to share sale prices in certain contexts. This creates challenges for automated online valuations, though a licensed appraiser working with MLS data and direct market research is not nearly as limited. Homes that have sat longer than expected on the market also raise questions for appraisers, and understanding why homes stay on the market in Southern California can help buyers and sellers contextualize unusual comp patterns.

Other common complications include:

- A property straddling two neighborhoods with very different price levels

- Unpermitted additions that inflate the perceived square footage

- Solar panel lease agreements that may or may not transfer value to the next owner

- HOA fees that affect the income approach for condo or townhome appraisals

What's driving home values in SoCal in 2026?

Appraisals do not happen in a vacuum. They are anchored to market conditions, and Southern California's 2026 housing landscape is shaping appraised values in some specific and meaningful ways.

The California median home price forecast for 2026 is approximately $905,000, representing a 3.6% year-over-year increase, with sales volume expected to climb about 2% and housing affordability hovering around 18%. That affordability figure means only about one in five California households can comfortably afford a median-priced home. That context is critical.

When affordability is that constrained, appraisals become a pressure valve. Lenders cannot afford to overlend on a declining or stagnant asset, so they rely even more heavily on rigorous appraisals. Buyers who stretch to afford a home in this market have very little cushion if the appraisal comes in low.

Key trends shaping appraised values in 2026:

- Limited inventory. Fewer homes for sale means less comp data and more upward pressure on prices, which can make appraiser adjustments more challenging to justify.

- Interest rate sensitivity. Higher mortgage rates reduce buyer purchasing power, which softens demand and can slow price growth, flattening the upward momentum appraisers would otherwise factor in.

- New ADU supply. California's ADU-friendly legislation has added thousands of units across SoCal, which are beginning to appear as comps and shift how appraisers treat ADU value adjustments.

- Insurance and natural disaster risk. Properties in fire-prone zones or flood plains increasingly face insurance challenges that affect buyer demand and, by extension, market value.

You can dig deeper into the data and projections with our coverage of SoCal market trends 2026, which connects neighborhood-level data to broader regional forces. For investors specifically, the LA and OC investment tips resource outlines how to factor appraisal risk into acquisition strategy.

SoCal's market moves faster and with more local variation than most markets in the United States. An appraiser working in Los Angeles has to account for micro-trends that simply do not exist in Dallas or Phoenix. That is both a challenge and an opportunity for buyers and sellers who take the time to understand how valuation actually works here.

The real story: why accurate appraisals make (or break) SoCal deals

After walking through the mechanics, the methods, and the market context, here is the candid take on what we actually see in Southern California transactions.

The biggest mistake buyers and sellers make is treating price per square foot as a reliable shortcut. It is not. Price per square foot ignores lot premium, view corridors, functional floor plans, the quality of finishes, and the condition of major systems. Two homes on the same street can have dramatically different per-square-foot values for legitimate reasons, and an appraiser who understands SoCal will capture that nuance. One who does not will produce a report that is technically compliant but functionally misleading.

Expert appraisers use statistical methods including regression analysis with R-squared coefficients to justify adjustments for unique features like views and ADUs. This means that if a seller is counting on ocean-view premiums or an ADU to push their value higher, they need strong, recent, comparable evidence to back it up. Gut feeling does not show up in a USPAP-compliant report.

The fairness issue in appraisals is real and worth acknowledging. Research has shown that racial and neighborhood biases can influence valuations, and regulatory bodies including the FDIC and state appraisal boards are actively working to address it. Buyers in historically undervalued neighborhoods should know they have the right to challenge an appraisal if they believe the comp selection or adjustments reflect bias rather than market reality. The tools to do that, including requesting a reconsideration of value with new comps, are available and effective when used correctly.

Our experience in markets from Inglewood to Irvine shows that buyers and sellers who understand the appraisal process consistently negotiate smarter. A seller who anticipates a low appraisal can gather supporting comp data before listing. A buyer who understands how adjustments work can evaluate whether an appraiser missed a critical feature. These are not advanced skills. They are simply informed ones. Knowing the right SoCal negotiation strategies before you enter a deal can turn appraisal results from a crisis into a conversation.

The bottom line is this: the gap between what someone is willing to pay and what a home is worth on paper is where deals succeed or fall apart. Southern California's prices make that gap expensive. Understanding appraisals is not optional in this market. It is essential.

Ready to make your next move? Get local expertise

Knowing how appraisals work is only the beginning. Putting that knowledge to work requires real market data, local expertise, and a strategic partner who knows the difference between a strong comp and a misleading one.

At IN Realtors, we specialize in the Los Angeles, Orange County, and surrounding Southern California markets, and we bring that hyperlocal knowledge to every transaction. Whether you are buying for the first time or selling a property you have held for decades, the appraisal outcome depends heavily on preparation and positioning. Browse current listings in Southern California to see what is active in your target area, request a free home valuation to understand what your property is worth before you list, and connect with us for expert selling support that goes beyond the sign in the yard. We are here to make sure the appraised value reflects the true story of your home.

Frequently asked questions

How long does a home appraisal in Southern California take?

Most appraisals are completed within 5 to 10 business days from the date the on-site inspection is conducted, though unique or complex properties may take longer due to limited comp data.

Can the appraised value be different from the purchase price?

Yes, and it happens regularly. The appraised value can be higher or lower than the agreed purchase price, which directly affects how much a lender will finance and what buyers or sellers may need to renegotiate.

What happens if an appraisal comes in low?

Buyers and sellers typically have three options: renegotiate the purchase price downward, have the buyer cover the gap in cash above the loan amount, or challenge the appraisal by submitting additional comparable sales through a formal reconsideration of value request.

Are online home valuations accurate in Southern California?

Automated valuations struggle significantly with unique properties and rapidly shifting SoCal conditions. Non-disclosure challenges and thin data limit automated models, while a licensed appraiser conducting a full on-site inspection provides far greater accuracy.

How does the 2026 housing market outlook affect appraisals?

With California's median price forecast at $905K and affordability sitting at roughly 18%, lenders are leaning harder on accurate appraisals, making it more important than ever for buyers and sellers to understand how appraised values are determined and challenged.