TL;DR:

- Down payment assistance in West Covina offers first-time buyers grants and deferred loans up to $100,000. Eligibility depends on income, credit, first-time buyer status, and completing HUD-approved education before applying through participating lenders. Repayment varies, with grants needing no repayment and deferred loans requiring shared equity repayment upon selling or refinancing.

Down payment assistance in West Covina is defined as financial aid provided to eligible first-time homebuyers to cover part or all of their down payment and closing costs when purchasing a home. Los Angeles County alone offers 52 active DPA programs, including grants and deferred loans that can provide up to $100,000 toward a purchase. Programs like the LACDA Home Ownership Program, CalHFA MyHome Assistance Program, and GSFA Platinum each serve buyers in West Covina with different funding structures and eligibility rules. The industry standard term for this category of aid is "down payment assistance," often abbreviated as DPA. Understanding which program fits your situation is the difference between waiting years to save or buying a home this year.

What down payment assistance programs are available in west covina?

West Covina buyers have access to several well-funded DPA programs at the county, state, and private levels. The most realistic funding stacks for local buyers range between $20,000 and $80,000, with the top county program reaching $100,000. Knowing the structure of each program helps you decide which to pursue first.

LACDA home ownership program

The Los Angeles County Development Authority (LACDA) Home Ownership Program is the most substantial local option. It provides up to $100,000 or 20% of the purchase price, whichever is less, as a deferred second loan. The loan carries zero percent interest and requires no monthly payments. Repayment is triggered only when you sell, refinance, or move out of the home. This structure makes it one of the most buyer-friendly programs available in Southern California.

CalHFA MyHome assistance program

The California Housing Finance Agency (CalHFA) offers the MyHome Assistance Program as a deferred-payment junior loan. It provides up to 3.5% of the purchase price for FHA loans and up to 3% for conventional loans. CalHFA MyHome is designed to stack on top of a CalHFA first mortgage, which means you apply for both through the same participating lender. This program is particularly useful for buyers who need help covering the gap between their savings and the required down payment.

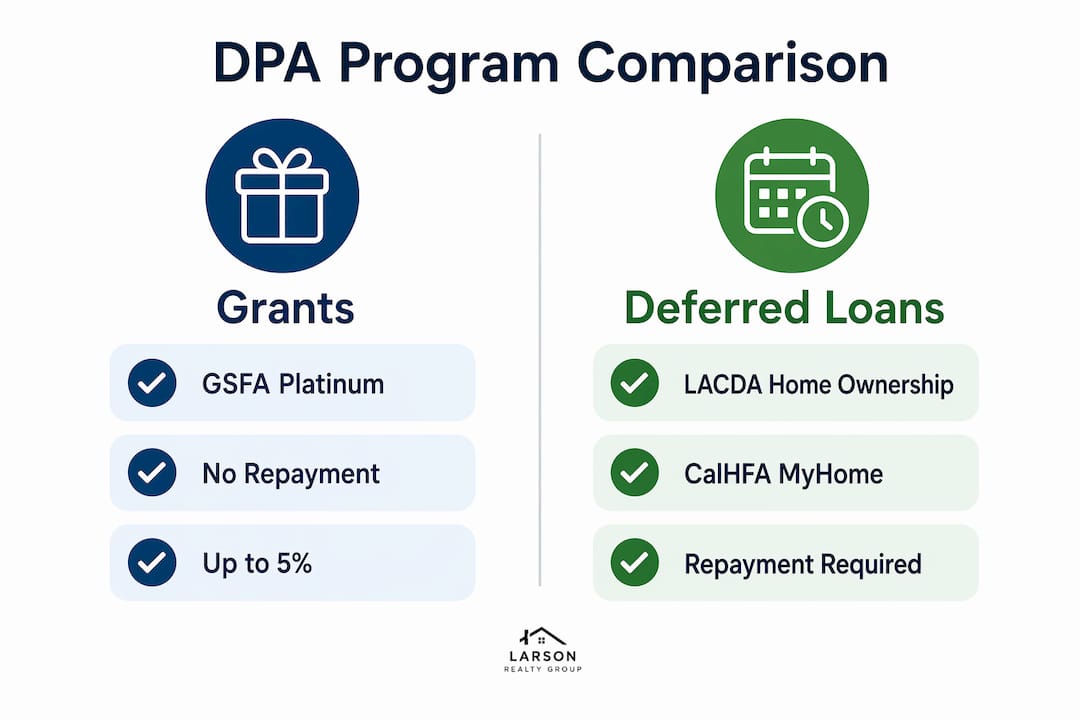

GSFA platinum and private sector options

The Golden State Finance Authority (GSFA) Platinum program offers a grant of up to 5% of the loan amount. Unlike the LACDA and CalHFA programs, grant-based programs like GSFA Platinum require no repayment at all, though they carry income and occupancy restrictions. The Bank of America Down Payment Grant and the LA County Greenline Home Program are two additional grant options worth exploring. For buyers who want a private-sector complement to government aid, First City Credit Union offers first-time homebuyer mortgage programs with down payments as low as 3%, which can be combined with county or state grants to maximize purchasing power.

Program comparison at a glance

| Program | Assistance Type | Maximum Amount | Repayment Required |

|---|---|---|---|

| LACDA Home Ownership | Deferred Loan | $100,000 or 20% | Yes, upon sale or refinance |

| CalHFA MyHome | Deferred Loan | 3%–3.5% of price | Yes, upon sale or refinance |

| GSFA Platinum | Grant | Up to 5% of loan | No |

| Bank of America Grant | Grant | Up to $10,000 | No |

| First City Credit Union | Low Down Mortgage | 3% minimum down | Standard mortgage terms |

The key distinction is grants versus deferred loans. Grants require no repayment and reduce your long-term financial obligation. Deferred loans delay repayment but do not eliminate it. Buyers who qualify for both types should prioritize grants first, then layer in deferred loans to cover the remaining gap. For a broader look at low down payment options across California, the Increaltors blog covers the full range of programs available in 2026.

How do you qualify for down payment assistance in west covina?

Qualifying for DPA in West Covina requires meeting several specific criteria set by each program. Most programs share a common baseline, though individual rules vary. Here is what you need to meet before applying.

First-time homebuyer status. Applicants must not have owned a home in the past three years. This applies to all borrowers on the loan, not just the primary applicant. If your spouse owned a home two years ago, you may not qualify under most programs.

Income limits. Each program sets income caps relative to the Area Median Income (AMI) for Los Angeles County. LACDA and CalHFA both require your household income to fall below a set threshold, which changes annually. Exceeding the limit by even a small amount disqualifies you, so verify current figures with your lender before applying.

Occupancy requirement. You must intend to occupy the purchased home as your principal residence. Investment properties and vacation homes do not qualify. The LACDA program requires you to live in the home continuously, and moving out triggers repayment of the deferred loan.

Minimum personal contribution. The LACDA program requires a minimum personal investment of 1% of the purchase price from your own funds. This cannot come from a gift. On a $600,000 home, that means $6,000 from your own savings, regardless of how much assistance you receive.

Credit score. Most DPA programs require a minimum credit score of 600 to qualify. Some programs, including CalHFA conventional options, may require higher scores. Check your credit report at least three months before applying so you have time to address any errors or derogatory marks.

HUD-approved homebuyer education. Every major DPA program in Los Angeles County requires completion of an 8-hour HUD-approved homebuyer education seminar. This is not optional. Skipping it stops your application entirely.

Pro Tip: Complete the HUD-approved education seminar before you start house hunting. The certificate is required for lender processing, and waiting until you find a home can cost you funding if the program runs out of money first.

The Increaltors guide on first-time buyer tips for Southern California covers additional preparation steps that apply directly to West Covina buyers.

What is the step-by-step process to apply for DPA?

The application process for down payment assistance in West Covina follows a specific sequence. Skipping steps or applying out of order is the most common reason buyers lose funding. Follow this process exactly.

-

Check your eligibility. Review income limits, credit score requirements, and first-time buyer status before doing anything else. Use the LACDA and CalHFA websites to confirm current thresholds.

-

Complete the HUD-approved education seminar. Applicants must complete the 8-hour seminar before lenders can process funding approval. Register early. Many classes fill up weeks in advance, especially in the San Gabriel Valley area.

-

Get mortgage pre-approval through a participating lender. DPA applications go through participating lenders, not directly to government offices. Your lender verifies income eligibility and checks current funding availability. Not every lender participates in every program, so confirm program participation before committing to a lender.

-

Submit your DPA application through your lender. Applications are processed on a first-come, first-served basis. Programs can exhaust their funding within weeks of a new allocation. Your lender submits the application on your behalf once you are under contract on a home.

-

Gather required documentation. Expect to provide two years of tax returns, recent pay stubs, bank statements showing your 1% personal contribution, the HUD education certificate, and a signed purchase agreement.

-

Manage timing carefully. The gap between application submission and funding approval can take several weeks. Coordinate your closing date with your lender to avoid delays. A misaligned timeline is one of the most common pitfalls in the DPA process.

Pro Tip: Ask your lender specifically which DPA programs they are currently approved to process. Some lenders are certified for LACDA but not CalHFA, and vice versa. Working with a lender approved for multiple programs gives you more options.

| Application Stage | Key Action | Common Pitfall |

|---|---|---|

| Pre-application | Complete HUD seminar | Waiting until after finding a home |

| Pre-approval | Confirm lender participation | Choosing a non-participating lender |

| Application submission | Submit through lender only | Applying directly to government office |

| Documentation | Provide all required financial records | Missing the 1% personal contribution proof |

| Closing coordination | Align DPA funding with closing date | Scheduling closing before funds are confirmed |

The Increaltors guide on buying a house in LA walks through the full homebuying process in detail, including how DPA fits into each stage.

What do first-time buyers need to know about DPA costs and repayment?

Down payment assistance is not free money in every case. Understanding the financial obligations attached to DPA programs protects you from surprises years down the road.

Closing costs are separate from DPA. Closing costs range from 2% to 6% of the loan amount and include appraisal fees, title insurance, escrow fees, and lender charges. On a $600,000 purchase, that is $12,000 to $36,000 in costs that DPA typically does not cover. Budget for these independently.

Deferred loans are still liens. The LACDA program and CalHFA MyHome are secured by a second Deed of Trust on your property. This means the loan is a legal claim against your home. Zero percent interest and no monthly payments make it manageable, but it is not forgiven.

Shared equity means you owe more than you borrowed. When you sell or refinance, repayment includes the original loan amount plus a share of the home's appreciation. If your home gained $200,000 in value and the program holds a 20% equity share, you owe $40,000 on top of the original loan balance. This is the most misunderstood aspect of deferred DPA loans.

Repayment triggers to know:

- Selling the home at any point

- Refinancing the first mortgage

- Moving out and converting to a rental

- Transferring title to another party

"DPA programs unlock homeownership but come with financial commitments like shared equity, which buyers must understand fully before signing." LACDA Program Administrator Insight

Plan your long-term finances with the repayment obligation in mind. If you expect to sell within five years, calculate the shared equity payback against your projected appreciation before deciding how much DPA to accept. For buyers who want to avoid repayment entirely, prioritizing grant-based programs like GSFA Platinum is the smarter move.

Key takeaways

Down payment assistance in West Covina gives first-time buyers access to up to $100,000 in funding, but the programs require careful preparation, precise timing, and a clear understanding of repayment obligations.

| Point | Details |

|---|---|

| Multiple programs available | LACDA, CalHFA MyHome, and GSFA Platinum each serve West Covina buyers with different funding structures. |

| Education seminar is mandatory | Complete the 8-hour HUD-approved seminar before applying to avoid losing funding to faster applicants. |

| Apply through lenders only | DPA submissions go through participating lenders, not government offices directly. |

| Grants beat deferred loans | Grant-based programs like GSFA Platinum require no repayment and reduce long-term financial obligations. |

| Shared equity affects resale | Deferred loans are repaid with an appreciation share upon sale or refinance, so factor this into long-term planning. |

What i've learned after years of helping west covina buyers navigate DPA

The biggest mistake I see first-time buyers make is treating DPA as an afterthought. They find a home they love, then scramble to figure out assistance. By that point, the HUD seminar hasn't been completed, the lender isn't participating in the right program, and the funding window has closed. The buyers who succeed are the ones who treat the education seminar and lender selection as step one, not step five.

I've also seen buyers leave money on the table by applying to only one program. Combining private credit union loans with government grants can cover most of the down payment gap for buyers who qualify for both. It takes more coordination, but the payoff is real. A buyer who stacks a GSFA Platinum grant with a LACDA deferred loan can walk into a West Covina home with minimal out-of-pocket costs beyond the required 1% personal contribution.

The shared equity clause in LACDA loans surprises people at closing. I always walk buyers through the math before they sign. If you plan to stay in the home for 10 or more years, the shared equity payback is a reasonable trade for the upfront help. If you plan to move in three years, the math may not work in your favor. Know your timeline before you commit.

One more thing: the West Covina market moves fast. Homes in the San Gabriel Valley regularly attract multiple offers. Getting your DPA pre-approval and education certificate done early means you can write a competitive offer without waiting on paperwork. The buyers I've seen win in this market are prepared before the right home appears, not after. The Increaltors West Covina buying guide covers local market conditions in detail if you want to understand what you're competing against.

— Irvin Nierras

Start your west covina home search with the right support

Finding the right home and the right assistance program at the same time requires local expertise. Increaltors works with first-time buyers across West Covina and the greater Los Angeles area, connecting you with homes that fit your budget and timeline.

Whether you're looking for a single-family home with room to grow or a lower-maintenance condo that fits a first-time buyer's budget, Increaltors has current listings across West Covina and surrounding communities. Starting your home search early gives you time to align your DPA application with your closing timeline, which is one of the most important factors in securing funding. Browse the full homes for sale inventory today and connect with Irvin Nierras to get matched with properties that work with your assistance program.

FAQ

What is the maximum DPA amount available in west covina?

The LACDA Home Ownership Program provides up to $100,000 or 20% of the purchase price, whichever is less. Most buyers in Los Angeles County receive between $20,000 and $80,000 depending on the program and purchase price.

Do i need to repay down payment assistance in west covina?

It depends on the program. Grant-based programs like GSFA Platinum require no repayment. Deferred loan programs like LACDA and CalHFA MyHome require repayment upon sale, refinance, or moving out, and LACDA includes a shared equity component tied to home appreciation.

What credit score do i need for DPA programs in west covina?

Most programs require a minimum credit score of 600. Some CalHFA conventional loan options may require higher scores. Check your credit at least three months before applying to allow time for corrections.

Can i combine multiple DPA programs in west covina?

Yes. Buyers can stack programs such as a GSFA Platinum grant with a LACDA deferred loan or combine a First City Credit Union mortgage with state assistance. Combining programs increases your total funding and reduces out-of-pocket costs.

Where do i apply for down payment assistance in west covina?

You apply through a participating lender, not directly through a government office. Your lender verifies eligibility, checks current funding availability, and submits the application on your behalf. Confirm that your lender is approved for the specific program you want before starting the process.